Artificial Intelligence for Aviation Law Market Research Report

The lawyer still owns judgment. The machine takes a growing share of the repetitive lift.

1. Executive Summary

Aviation law is one of the legal market’s better test cases for AI disruption because the work is so information-heavy. Lawyers in this niche deal with regulatory filings, aircraft leasing documents, safety investigations, accident claims, insurance coverage, passenger and cargo disputes, FAA and DOT compliance, drone rules, cross-border contracts and litigation records that can run for thousands of pages. It is not simple work. It is specialized, technical and often high-stakes.

That is exactly why AI matters here.

The core opportunity is not “robots replacing aviation lawyers.” That framing is too blunt and, frankly, not very useful. The real shift is more practical: AI will compress research time, speed up first drafts, surface regulatory changes faster, triage claims earlier, review aviation contracts at scale and give clients more visibility into pricing. The lawyer still owns judgment. The machine takes a growing share of the repetitive lift.

Definition of the sub-category

“Artificial Intelligence for Aviation Law” means AI-enabled software, workflows and data systems used to support legal services tied to airlines, airports, aircraft owners and lessors, manufacturers, MRO providers, insurers, drone operators, advanced air mobility companies, cargo carriers, passengers, aviation employees and public agencies. It includes generative AI, legal research AI, contract review, litigation analytics, compliance monitoring, intake automation, discovery tools, knowledge management and AI-assisted pricing.

Market size (U.S. + global)

The aviation-law revenue pool is not separately reported in most public legal-industry datasets, so the market-size figures in this report are modeled estimates. The base-case estimate places the U.S. aviation-law market at roughly $1.35 billion in annual legal revenue in 2026, with a plausible range of $0.9 billion to $2.1 billion. The global market is estimated at roughly $3.8 billion, with a plausible range of $2.5 billion to $5.8 billion. These figures are built from attorney population estimates, public legal-market data, aviation-sector activity, practice-area mix assumptions and revenue-per-lawyer benchmarks. Broader market anchors include reported U.S. legal services market revenue, global legal services revenue and legal AI market forecasts.

Estimated current AI penetration (% of firms using AI)

Current AI adoption in aviation law appears uneven. Large firms, in-house aviation teams and global practices are moving fastest because they already have the security infrastructure, data rooms, document systems and legal operations staff needed to control AI use. Smaller aviation boutiques may be experimenting, but formal deployment is less consistent. The base-case estimate used here is that about 32 percent of aviation-law practitioners regularly use AI in some part of their work in 2026. This is not presented as a dedicated aviation-law survey result. It is a modeled estimate based on broader legal AI adoption surveys and adjusted for the profile of aviation-law work.

Core AI disruption vectors

The most important disruption vectors are:

- Research compression. AI can reduce the time needed to scan aviation statutes, agency guidance, enforcement materials, case law and prior work product.

- Drafting acceleration. Memos, pleadings, claim summaries, contract markups, regulatory comment drafts and client updates can move from blank page to reviewable draft much faster.

- Contract and lease review. Aircraft purchase agreements, operating leases, maintenance contracts, airport agreements and insurance documents are strong candidates for AI-assisted review.

- Claims and litigation analytics. Accident files, passenger claims, cargo disputes and insurance matters can be sorted, summarized and assessed earlier in the matter lifecycle.

- Compliance monitoring. AI can track changes from agencies such as the FAA, DOT, TSA, EASA and ICAO and push targeted alerts to legal teams.

- Pricing pressure. As clients see routine work move faster, they will push harder for fixed fees, capped fees, subscriptions and clearer value reporting.

Estimated automation potential (% of billable time)

The automation potential is significant, but it needs to be handled carefully. This report’s workflow model estimates that roughly 38 percent of aviation-law billable time is theoretically automatable or compressible. The practical near-term figure is lower, closer to 25 to 30 percent, because aviation lawyers still need to verify citations, protect privilege, apply judgment, supervise outputs and manage risk. In the first 12 to 18 months of a disciplined rollout, a realistic target is 10 to 15 percent effective time compression across selected workflows.

5-year outlook

The five-year outlook is clear: AI will become normal operating infrastructure for aviation-law practices. By 2030, the strongest firms will not simply “use AI.” They will have aviation-specific clause banks, regulatory trackers, litigation playbooks, accident-response templates, matter taxonomies, prompt libraries, review protocols and data-security rules. The advantage will come from combining AI tools with domain-specific legal knowledge.

Strategic risks if firms ignore AI

Firms that ignore AI face more than a productivity gap. They risk looking expensive, slow and hard to work with. They may lose RFPs, underperform on fixed-fee matters, overstaff routine work, frustrate younger lawyers and give in-house teams another reason to bring aviation work inside. The danger is not sudden collapse. It is margin erosion, one matter at a time.

Market Size Snapshot

(2026, modeled)

(2026, modeled)

(2024, reported)

(2030, forecast)

AI Adoption Curve (S-curve projection)

Revenue vs Automation Exposure

2. Definition & Market Scope

Aviation law is a narrow practice area with a wide operating footprint. It is not just “airline law.” It reaches across airlines, airports, aircraft leasing, aircraft finance, aviation insurance, manufacturers, maintenance providers, cargo operators, drone companies, advanced air mobility ventures, passengers, employees, federal agencies and cross-border regulators. The FAA’s own long-range forecasting framework treats aviation as a broad ecosystem that includes U.S. airline traffic, capacity, general aviation, commercial space, UAS, advanced air mobility and FAA workload, which is a useful way to frame the legal market as well. (Federal Aviation Administration)

That mix makes the category unusually attractive for AI. The work is specialized, but much of the raw material is structured or semi-structured: rules, contracts, filings, enforcement materials, incident records, correspondence, technical exhibits, claims files, case law and agency guidance. The FAA says its FY 2025-2045 Aerospace Forecast uses statistical models to explain and incorporate emerging aviation trends across different industry segments, which reinforces how data-heavy the aviation ecosystem has become. (Federal Aviation Administration)

Aviation law includes legal services where aviation-specific facts, regulations, industry documents or risk standards are central to the matter. It includes traditional aviation work and emerging aviation work, especially drones, commercial space-adjacent issues and advanced air mobility. The FAA’s emerging aviation entrants compendium focuses on unmanned aircraft systems and advanced air mobility because both have shown maturing operations or significant market potential, making them appropriate to include in the forward-looking scope of aviation law. (Federal Aviation Administration)

What qualifies as aviation law

Included in scope:

- Airline regulatory compliance

- FAA, DOT, TSA, NTSB and state aviation matters

- Aircraft finance, leasing, purchase and sale transactions

- Aircraft title, registration and lien issues

- Airport concessions, use agreements and infrastructure matters

- Aviation insurance and coverage disputes

- Passenger, baggage and cargo claims

- Accident litigation and incident response

- Product liability involving aircraft, engines, parts or aviation systems

- Maintenance, repair and overhaul contracts

- Drone, UAS and advanced air mobility regulatory work

- Aviation labor, employment and safety-sensitive workforce issues

- International aviation treaty and cross-border regulatory issues

- Aviation-related sanctions, export control and security reviews

- In-house legal operations for airlines, airports, lessors and aviation companies

Excluded or only partially included:

- General corporate work for an aviation client where no aviation-specific legal issue is involved

- Routine employment work for airlines unless aviation safety, union operations or regulatory issues are central

- Consumer travel complaints handled outside a legal workflow

- General real estate, tax or M&A work unless aviation assets, airport property or aviation regulation materially shape the matter

- Pure lobbying or public affairs work, unless tied to legal compliance or regulatory strategy

The practical rule is simple: if a matter requires aviation-specific legal knowledge, it belongs in the category. If the client happens to be an aviation company but the legal work could just as easily apply to a grocery chain or software company, it should be excluded or discounted.

Types of firms and legal teams serving the market

The aviation-law market is fragmented, but not evenly fragmented. A relatively small number of large firms handle the biggest aviation finance, airline restructuring, aircraft leasing, product liability and cross-border regulatory matters. A larger group of boutiques and regional firms handle accident litigation, insurance defense, passenger claims, airport matters, drone counseling and owner-operator work. This provider mix is modeled for this report rather than taken from a single public aviation-law census.

- Global and AmLaw firms

Global and AmLaw firms are positioned for high-value aviation finance, aircraft leasing, airline restructuring, complex product liability, large accident litigation, international regulatory work and major airport or infrastructure transactions. Their client base typically includes airlines, manufacturers, lessors, insurers, airports, private equity sponsors and multinational aviation companies.

These firms are also the most likely to have formal AI governance, secure legal-research tools, document automation teams and legal operations support. That matters because legal AI adoption in aviation law is not just about access to a model. It is about whether the firm can protect confidentiality, control work product, validate outputs and make AI fit inside existing matter workflows.

- Aviation boutiques

Boutiques are a major force in this niche. Many have deep subject-matter credibility and long-standing relationships with insurers, aircraft owners, operators, lessors, airports and aviation trade groups. They may not have the technology budget of a global firm, but they often have something equally valuable: repeat work, narrow expertise and strong templates.

For AI adoption, boutiques are a fascinating group. The right tool can give them scale without making them look generic. In a specialist market, speed matters, but credibility matters more.

- Mid-market and regional firms

Mid-market and regional firms often handle aviation matters tied to local airports, state aviation businesses, claims, insurance defense, employment, construction, municipal airport operations and regional airline issues. This segment matters because aviation legal demand follows physical aviation activity. Airports, maintenance facilities, cargo hubs, aerospace suppliers and business aviation operators all create legal work near where they operate.

Airport activity data supports that point. ACI-NA’s 2024 North American Airport Traffic Report covers passenger, freight/mail and aircraft operations data from 283 North American airports, showing that aviation activity is distributed across a broad operating network rather than concentrated only in a few airline headquarters cities. (ACI North America)

- Solo and small firms

Solo and small firms tend to appear in passenger claims, personal injury, owner-pilot disputes, aircraft purchase disputes, FAA certificate actions and smaller commercial conflicts. They may not account for a large share of total revenue, but they matter for access, claimant representation and long-tail aviation disputes.

- In-house aviation legal departments

Airlines, airports, manufacturers, lessors, insurers, drone companies, cargo carriers and aviation technology providers all maintain in-house legal capacity. In-house teams are not counted as external law-firm revenue, but they are central to the AI opportunity because they decide what gets sent outside, what stays internal and what can be automated.

AI could shift more aviation work in-house, especially routine research, first-pass contract review, regulatory monitoring, claims triage and outside counsel management. The FAA’s forecast work highlights UAS and advanced air mobility as maturing or high-potential aviation categories, which suggests that in-house demand will not come only from traditional airlines and airports over the next decade. (Federal Aviation Administration)

- ALSPs, legal operations teams and adjacent compliance vendors

Alternative legal service providers and compliance vendors are still a smaller part of aviation law than they are in discovery-heavy commercial litigation or contract lifecycle management. That may change. Aviation has enough recurring document review, regulatory monitoring, claims processing and contract analysis to support more specialized legal operations offerings.

Revenue model

Aviation law uses several revenue models, often within the same client relationship.

Hourly billing remains the dominant model for complex regulatory advice, aircraft finance, litigation, accident response, government investigations and bespoke contract work. This model is most exposed to AI-driven time compression because clients will eventually ask why a task that once took 12 hours still costs 12 hours when an AI-assisted workflow can produce a strong first pass in less time.

Contingency or success-fee economics appear most often in plaintiff-side accident litigation, passenger injury matters, cargo loss claims and certain commercial disputes. AI affects this model differently. Instead of directly reducing revenue, it can improve case screening, lower cost per matter, speed up demand packages and allow firms to handle a larger portfolio.

Flat-fee and capped-fee work is common in repeatable aviation contracts, entity and ownership support, aircraft purchase documentation, FAA registration assistance, certain drone advisory packages and compliance projects. AI is especially favorable here because time savings can flow to margin rather than automatically reducing billings.

Subscription and retainer models are still underdeveloped, but they are likely to grow. Good candidates include drone operators, charter companies, aviation startups, airport vendors, small fleet operators, maintenance providers and private aircraft ownership groups that need recurring legal updates but cannot justify constant hourly work.

Hybrid models are common for sophisticated aviation clients. A firm may charge hourly for high-risk legal judgment, fixed fees for repeat documentation, subscriptions for monitoring and success fees for certain disputes or transactions.

Attorney population and market-size estimates

The ABA reported that the U.S. lawyer population increased in 2025 and identified 1,374,720 resident active lawyers, up from 1,355,963 in 2024. (2Civility) The ABA’s lawyer population data is collected from state licensing bodies, which makes it a strong anchor for sizing a specialty practice population even though it does not publish a dedicated aviation-law attorney count. (American Bar Association)

Because there is no clean public aviation-law headcount, the niche population in this report is modeled rather than directly reported.

Base-case U.S. estimate:

Core aviation-law full-time-equivalent attorneys: 1,350

Broader attorney population touching aviation-law work: 2,750

Modeled range: 1,900 to 4,200 attorneys

Share of U.S. active lawyer population: roughly 0.14 percent to 0.31 percent

Base-case external U.S. aviation-law revenue pool: $1.35 billion

Modeled U.S. revenue range: $0.9 billion to $2.1 billion

Base-case global aviation-law revenue pool: $3.8 billion

Modeled global revenue range: $2.5 billion to $5.8 billion

The difference between “core FTE attorneys” and “attorneys touching aviation law” matters. Many lawyers do not spend all year on aviation matters. A litigation partner may handle one aviation product case and several non-aviation cases. A finance associate may work on aircraft leasing for six months and general asset finance for the rest of the year. The model converts partial participation into an aviation-law full-time-equivalent estimate, then uses a broader headcount estimate for adoption and workflow analysis.

The broader U.S. legal services market provides the anchor for the revenue model. Grand View Research estimated the U.S. legal services market at $396.80 billion in 2024 and projected a 2.5 percent CAGR from 2025 to 2030. (Grand View Research) Aviation law represents only a small slice of that market, but it is a high-value niche because the work is technical, risk-sensitive and often tied to large commercial assets.

Average revenue per attorney

The base model implies two revenue-per-lawyer views:

Revenue per broader aviation-law attorney: approximately $491,000

Revenue per core aviation-law FTE attorney: approximately $1.0 million

The first figure is better for measuring the real population of lawyers who may touch the work. The second figure is better for sizing the economic engine of the practice area because it reflects concentrated aviation-law capacity.

Both figures should be treated as modeled averages, not survey results. The real spread is wide. A senior partner at a global firm handling aircraft leasing or major product liability may generate several million dollars in annual working-attorney revenue. A solo lawyer handling certificate defense or smaller owner disputes may generate a much lower aviation-specific revenue figure.

Average billable hours

The model assumes an average of 1,650 billable or revenue-producing hours per aviation-law attorney-equivalent per year, with a practical range of 1,450 to 1,900 hours depending on role, firm size and matter type.

Large-firm associates and partners assigned to major disputes, aircraft finance transactions and regulatory projects may sit near the high end. In-house lawyers, solo lawyers, government-adjacent practitioners and lawyers with mixed practices may sit lower when measured only by aviation-law work.

Geographic distribution

Aviation-law demand is geographically clustered around four things:

- Major airline and airport hubs

- Regulatory centers

- Aerospace manufacturing and supplier corridors

- Business aviation, cargo and aircraft ownership activity

The strongest U.S. aviation-law markets include New York, Washington, D.C. and Northern Virginia, Dallas-Fort Worth, Miami and South Florida, Los Angeles and Southern California, Chicago, Atlanta, Seattle, Denver, Houston, San Francisco and Boston. This concentration is partly legal-market driven and partly aviation-activity driven. ACI-NA reported that the top 2024 North American airports by passenger traffic included Atlanta, Dallas-Fort Worth, Denver, Chicago O’Hare and Los Angeles, while the top cargo airports included Memphis, Anchorage, Louisville, Miami and Los Angeles. (ACI North America)

Washington, D.C. is central because of FAA, DOT, TSA, NTSB and federal regulatory work. New York is important for finance, leasing, insurance and global transactions. Texas, Florida and California combine aviation operations, business aviation, litigation, aircraft ownership and large legal markets. The ABA’s 2025 lawyer-population reporting also shows the importance of large legal markets such as California, Texas and Florida within their regions, which supports their inclusion as aviation-law concentration zones when combined with aviation activity. (PublicNow)

The market is not limited to these places. Every state with airports, aircraft owners, charter operators, maintenance facilities or drone operations has some aviation legal demand. The issue is concentration. The highest-value, most AI-addressable work tends to cluster where aviation activity and sophisticated legal buyers overlap.

Firm Size Distribution

Revenue Breakdown by Firm Tier

Geographic Concentration Heat Map

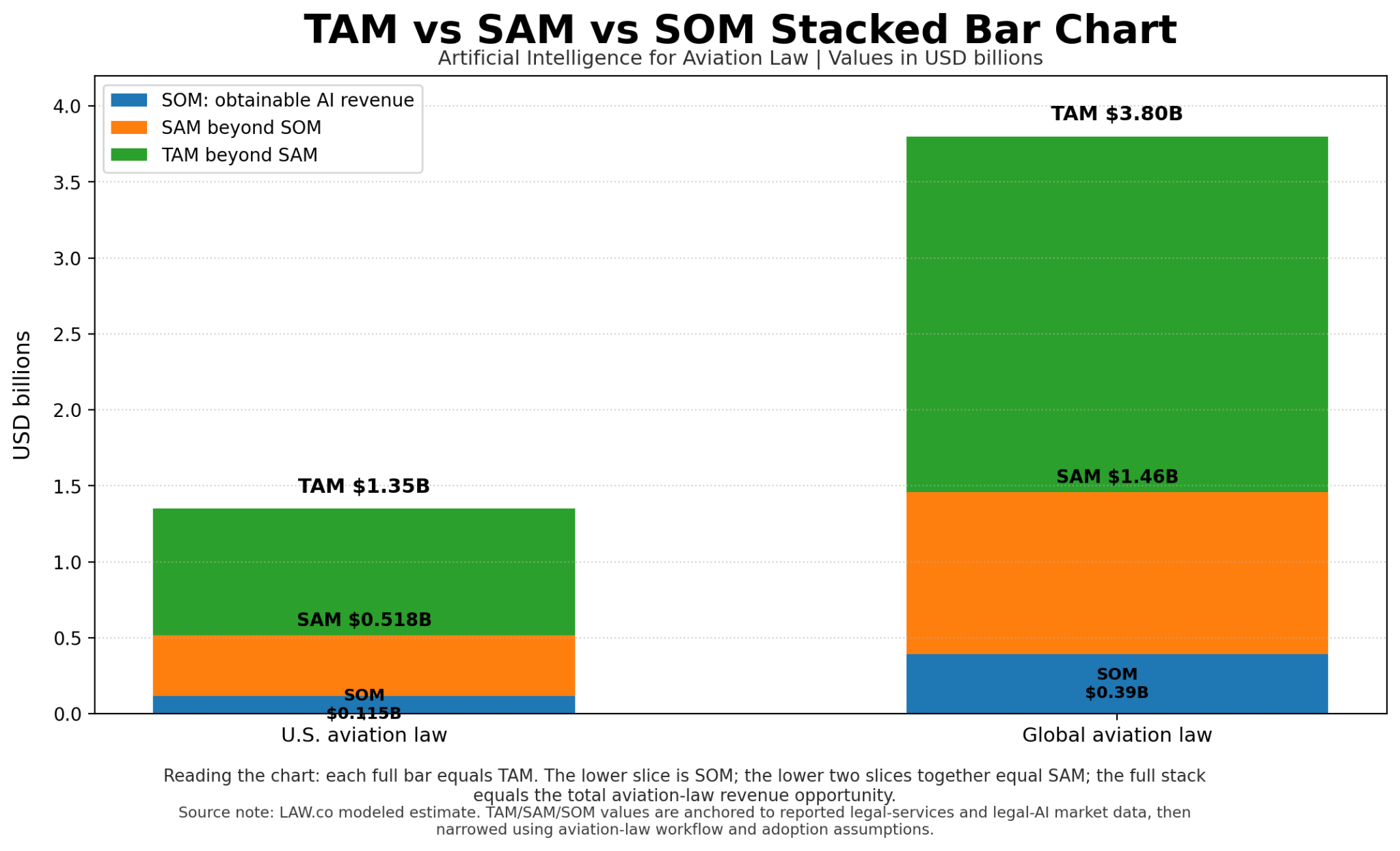

3. Total Addressable Market, SAM and SOM

This section sizes the economic opportunity for AI in aviation law from three angles: total legal-service revenue, the portion of that work that AI can realistically touch, and the portion vendors or AI-enabled legal providers can plausibly capture over the next five to ten years.

Aviation law is not a giant category by legal-market standards, but it is a high-value niche with unusually strong AI fit. It is document-heavy, regulation-heavy, deadline-heavy and often tied to expensive assets. That makes the category small enough for specialized vendors to understand, but valuable enough to justify purpose-built tools.

The broader market context matters. Grand View Research estimated the U.S. legal services market at $396.80 billion in 2024 and projected a 2.5 percent CAGR from 2025 to 2030. It also estimated the global legal services market at $1.0529 trillion in 2024, with projected growth to $1.3756 trillion by 2030. Aviation law is only a small slice of those markets, but it sits inside a large legal economy that is already being reshaped by AI, automation and alternative pricing pressure. (Grand View Research, Grand View Research)

The legal AI market is also growing quickly. Grand View Research estimated the global legal AI market at $1.45 billion in 2024 and projected it to reach $3.90 billion by 2030, a 17.3 percent CAGR from 2025 to 2030. The same source points to eDiscovery, case prediction, regulatory compliance, contract review and contract management as important legal AI use cases, all of which map closely to aviation-law workflows. (Grand View Research)

Market-sizing logic

The model uses three related market definitions.

TAM, or total addressable market, is the full aviation-law legal-services revenue pool. This is the revenue generated by firms and external legal-service providers for aviation-specific work, before any AI filter is applied.

SAM, or serviceable available market, is the portion of aviation-law work that AI tools can realistically support, accelerate, automate or compress. This does not mean AI replaces the lawyer. It means AI can affect the cost structure, speed, staffing or pricing of that work.

SOM, or serviceable obtainable market, is the portion of SAM that AI vendors, AI-enabled law firms, alternative legal service providers or legal operations teams can plausibly capture over five to ten years.

The model treats public legal-services and legal-AI market reports as anchors, then narrows the estimate using aviation-law practice assumptions. Public sources do not provide a clean aviation-law revenue census, so the aviation-specific figures below are LAW.co-modeled estimates rather than reported market totals. The broader legal-services anchors come from Grand View Research, while AI adoption and workflow assumptions are cross-checked against current legal AI market and professional-services AI adoption signals. (Grand View Research, Grand View Research, Grand View Research, Thomson Reuters)

TAM: total aviation-law revenue pool

Base-case TAM

U.S. aviation-law TAM, 2026 model: $1.35 billion

Global aviation-law TAM, 2026 model: $3.8 billion

Modeled U.S. range: $0.9 billion to $2.1 billion

Modeled global range: $2.5 billion to $5.8 billion

The U.S. TAM estimate is built from two methods. The first is an attorney productivity model: core aviation-law FTE attorneys multiplied by estimated revenue per lawyer. The second is a top-down share model: aviation-law revenue as a narrow percentage of the broader U.S. legal services market. The broader market anchor is Grand View Research’s U.S. legal services estimate of $396.80 billion in 2024. (Grand View Research)

TAM formula 1: attorney-driven model

Core aviation-law FTE attorneys × average aviation-law revenue per attorney = U.S. aviation-law TAM

1,350 core FTE attorneys × $1,000,000 average revenue per attorney = $1.35 billion

This figure should be read as an external legal-services revenue estimate, not a total cost-of-law estimate. It excludes a large amount of in-house legal labor at airlines, airports, manufacturers, lessors, insurers, cargo carriers, drone companies and aviation technology providers. That in-house layer matters for AI adoption because in-house teams may use AI to keep more routine work inside instead of sending it to outside counsel.

TAM formula 2: broader legal-market share model

U.S. legal services market × aviation-law share = U.S. aviation-law TAM

$396.80 billion × 0.34 percent = approximately $1.35 billion

The 0.34 percent share is a modeled assumption. It is designed to reflect aviation law’s status as a specialist category with high-value matters but a limited attorney population compared with larger areas such as corporate, employment, personal injury, real estate, tax, healthcare, insurance and commercial litigation.

The global TAM estimate uses the same logic, scaled against the global legal-services market. Grand View Research estimated the global legal services market at $1.0529 trillion in 2024 and projected $1.3756 trillion by 2030. The global aviation-law market is modeled at $3.8 billion in 2026, or roughly 0.34 percent to 0.38 percent of the global legal-services pool, adjusted for aviation activity, cross-border aircraft leasing, manufacturing, international regulatory work and global airline operations. (Grand View Research)

SAM: portion realistically addressable by AI tools

Base-case SAM

U.S. aviation-law structural SAM: $518 million

Global aviation-law structural SAM: $1.46 billion

Current practical U.S. SAM, 2026: $233 million

Current practical global SAM, 2026: $657 million

The structural SAM is the portion of aviation-law work that AI can theoretically support or compress based on workflow type. The model uses a weighted automation exposure of 38.4 percent across aviation-law activities. That figure comes from the workflow decomposition in Section 5, where tasks such as research, drafting, contract review, compliance monitoring, intake, discovery, matter reporting and billing are scored separately.

SAM formula

TAM × weighted automation exposure = structural SAM

U.S. structural SAM:

$1.35 billion × 38.4 percent = $518 million

Global structural SAM:

$3.8 billion × 38.4 percent = $1.46 billion

This is not a claim that 38.4 percent of aviation-law revenue disappears. It is a measure of work exposed to AI-driven compression, assistance or redesign. In hourly matters, that may create revenue pressure. In fixed-fee matters, it may improve margin. In contingency matters, it may increase case capacity. In in-house environments, it may reduce outside counsel dependency.

The model then applies a near-term readiness discount. Not every theoretically automatable workflow is immediately addressable. Aviation law has confidentiality concerns, aviation-safety sensitivity, privilege issues, cross-border data constraints and a high cost of error. Thomson Reuters’ 2025 report says about half of professionals across legal, tax, accounting, audit, risk, fraud and government use GenAI in some fashion, but many still rely on limited or general-purpose use rather than deeply embedded sector-specific workflows. (Thomson Reuters)

Current practical SAM formula

Structural SAM × readiness factor = current practical SAM

U.S. current practical SAM:

$518 million × 45 percent = $233 million

Global current practical SAM:

$1.46 billion × 45 percent = $657 million

The 45 percent readiness factor is a modeled estimate. It reflects the portion of exposed work that can be reached today through available legal AI tools, controlled workflows, secure research environments, contract analysis, eDiscovery platforms, compliance monitoring and supervised drafting. The rest is slower to address because it involves poor data hygiene, client approval barriers, risk-sensitive judgment, legacy systems or highly bespoke legal analysis.

SOM: likely capture over five to ten years

Base-case SOM

U.S. SOM, 2031 annual AI revenue opportunity: $115 million

Global SOM, 2031 annual AI revenue opportunity: $390 million

U.S. SOM range, 2031: $75 million to $155 million

Global SOM range, 2031: $260 million to $570 million

The SOM is smaller than the SAM because vendors and AI-enabled providers do not capture the full value of time saved. A law firm may use AI to protect margins. An in-house team may use it to reduce outside counsel spend. A vendor may capture subscription revenue, usage fees, implementation fees, data-cleaning fees, monitoring fees or managed-service revenue. Those are different revenue pools.

SOM formula

Structural SAM × monetization rate × adoption penetration = obtainable annual AI revenue

For the 2031 U.S. base case:

$518 million structural SAM × 30 percent monetization rate × 74 percent adoption penetration = approximately $115 million

For the 2031 global base case:

$1.46 billion structural SAM × 36 percent monetization rate × 74 percent adoption penetration = approximately $390 million

The higher global monetization assumption reflects a broader mix of enterprise legal departments, cross-border leasing, global regulatory monitoring, multinational investigations, and aviation contract portfolios. It also reflects the possibility that vendors package aviation-specific AI into broader enterprise legal, compliance, risk, contract lifecycle and eDiscovery platforms.

The adoption curve is consistent with broader market signals. Grand View Research forecasts the legal AI market growing from $1.45 billion in 2024 to $3.90 billion by 2030, and Thomson Reuters reports that GenAI use across professional sectors is already widespread enough to make adoption a near-term operating question rather than a distant theory. (Grand View Research, Thomson Reuters)

Billable-hours model

A second way to size the market is to model the billable-hour pool.

Base assumptions:

Core aviation-law FTE attorneys: 1,350

Average annual billable or revenue-producing hours per attorney: 1,650

Total modeled aviation-law hours: 2.23 million

Weighted automation exposure: 38.4 percent

AI-exposed hours: 855,000

Practical near-term AI-compressible hours: 558,000 to 669,000

Billable-hours formula

Attorneys × average annual billable hours = total aviation-law hours

1,350 × 1,650 = 2,227,500 hours

Total hours × weighted automation exposure = structurally AI-exposed hours

2,227,500 × 38.4 percent = 855,360 hours

AI-exposed hours × practical realization rate = near-term compressible hours

855,360 × 65 percent to 78 percent = 556,000 to 667,000 hours

The realization rate is lower than the theoretical automation exposure because aviation lawyers still need to verify citations, preserve privilege, check facts, handle client communications and apply human judgment. This is especially important in aviation, where a drafting error, regulatory misread or missed technical detail can create financial, safety or reputational risk.

Legal-tech spending per firm

The legal-tech spend pool is much smaller than the legal-services TAM, but it is the pool AI vendors can most directly capture. The legal AI market itself is still small relative to the broader legal-services market. Grand View Research estimated global legal AI revenue at $1.45 billion in 2024, compared with a global legal-services market above $1 trillion. That gap is the opening: AI software is a small spend category today, but it is targeting workflows inside a very large labor-driven industry. (Grand View Research, Grand View Research)

For aviation law, the model estimates 2026 U.S. AI-related spend at $22 million across law firms, in-house legal departments and adjacent legal operations providers. This includes AI legal research, contract review, eDiscovery analytics, compliance monitoring, knowledge management, workflow automation, implementation, training and governance support.

Modeled 2026 AI spend by provider type:

Global and AmLaw aviation practices: $10.6 million

Aviation boutiques: $4.8 million

Mid-market and regional firms: $3.1 million

In-house aviation legal departments: $2.4 million

Solo and small firms: $0.7 million

ALSPs and legal operations providers: $0.4 million

Total: $22.0 million

This spend allocation follows both revenue concentration and adoption readiness. Larger firms are expected to spend more because they have higher-value matters, more secure technology infrastructure, more client pressure and stronger incentives to protect margin. Boutiques have a lower total budget, but their aviation-specific knowledge makes them strong candidates for targeted tools.

Recent market behavior supports the view that large law firms are willing to make major AI investments when they believe the technology can reshape delivery economics. For example, the Financial Times reported in 2026 that Kirkland & Ellis plans to spend $500 million over several years building its own proprietary AI platform, including more than $100 million in 2026 alone. That is an extreme Big Law example, not a benchmark for aviation boutiques, but it shows how seriously top firms are treating AI as infrastructure. (Financial Times)

TAM vs SAM vs SOM

AI Spend Growth Forecast (5–10 year CAGR)

AI Budget Allocation by Firm Size

4. Current State of AI Adoption

AI adoption in aviation law is already underway, but it is uneven. The best way to think about the market is not “AI users versus non-users.” It is more layered than that.

Some lawyers are casually using general-purpose tools for brainstorming or first drafts. Some firms have approved legal-specific AI tools for research, document review or correspondence. A smaller group has embedded AI into matter workflows, pricing, regulatory monitoring, contract analysis or client reporting. The gap between those groups is where the market opportunity sits.

The broader legal market is moving quickly. Clio’s 2025 Legal Trends reporting found that 79 percent of legal professionals use AI, with large law firms reporting the highest adoption at 87 percent and solo firms still reporting meaningful use at 71 percent. The same report found that growing firms use automations and AI-supported workflows more heavily than stable or shrinking firms. (2Civility)

Other legal-industry surveys show a more cautious picture when the question is not “use AI at all,” but “use generative AI at work” or “firm-wide legal-specific AI adoption.” The 2025 Legal Industry Report, published through the ABA Law Practice Division and based on more than 2,800 legal professionals, found that 31 percent of respondents personally used generative AI at work, while law-firm use was 21 percent. It also found that firms with 51 or more lawyers reported 39 percent generative AI adoption, while firms with 50 or fewer lawyers were closer to 20 percent. (American Bar Association)

That spread matters for aviation law. Aviation practices are more likely than many small consumer-facing practices to have complex research, regulated documents and repeatable workflows. But they also face stricter concerns around confidentiality, privilege, aviation safety, regulatory accuracy and client approval. In short: the use case is strong, but the risk tolerance is lower.

Adoption baseline for aviation law

There is no public survey that cleanly measures AI adoption only among aviation-law firms. The numbers below are therefore modeled estimates, anchored to broader legal-industry adoption data from Clio, MyCase/ABA Law Practice Division, ACC/Everlaw, FTI/Relativity and ABA technology reporting.

Base-case aviation-law adoption estimate, 2026:

Regular or firm-sanctioned AI use in aviation-law workflows: 32 percent

Personal or informal generative AI experimentation: 55 percent

Legal research AI usage: 49 percent

Workflow automation usage: 34 percent

AI-assisted drafting usage: 41 percent

Contract review or document analysis AI usage: 29 percent

Predictive analytics usage: 14 percent

AI-assisted intake, claims triage or client communication usage: 18 percent

Compliance monitoring or regulatory alert AI usage: 22 percent

The 32 percent figure is the cleanest headline adoption estimate for aviation law because it focuses on regular or approved workflow use, not casual experimentation. It sits between the 21 percent law-firm use figure reported in the 2025 Legal Industry Report and the much higher 79 percent broad AI-use figure reported by Clio. That middle position is intentional. Aviation law has stronger AI fit than many general practices, but adoption is constrained by risk and client sensitivity. (American Bar Association, 2Civility)

Generative AI adoption

Generative AI is the most visible adoption category. It is also the messiest.

In aviation law, generative AI is most commonly used for:

- First drafts of client alerts

- Internal research summaries

- Chronologies

- Matter status updates

- Regulatory change summaries

- Deposition and interview prep outlines

- Claim summaries

- Contract issue lists

- Billing narratives

- Email and client correspondence drafts

The legal market is already using GenAI for many of these general tasks. The 2025 Legal Industry Report found that 54 percent of legal professionals use AI to draft correspondence, 14 percent use it to analyze firm data and matters, and 47 percent expressed interest in AI tools that help generate insights from firm financial data. (American Bar Association)

Modeled aviation-law GenAI adoption by segment, 2026:

Solo aviation lawyers: 18 percent firm-sanctioned or regular GenAI use

Small and SMB aviation firms, 2 to 50 lawyers: 24 percent

Mid-market aviation practices, 51 to 199 lawyers: 38 percent

AmLaw 200 and global aviation practices: 65 percent

In-house aviation legal departments: 52 percent

Overall aviation-law weighted estimate: 32 percent

The in-house figure is supported by broader corporate-law data. ACC and Everlaw reported in October 2025 that 52 percent of in-house counsel were actively using GenAI, more than double the 23 percent reported in 2024. The same ACC survey found that 91 percent cited efficiency as the most tangible benefit, especially in drafting and legal research. (Association of Corporate Counsel (ACC))

For large corporate legal departments, adoption may be even higher. FTI Consulting and Relativity reported in March 2026 that 87 percent of general counsel said their teams were using AI, up from 44 percent in 2025, with common use cases including summarization, contract-clause identification, transcription, foreign-language analysis and first-pass review. (FTI Consulting)

Workflow automation adoption

Workflow automation is less flashy than GenAI, but it may matter more economically. Aviation-law teams do not only need a writing assistant. They need repeatable systems for intake, matter tracking, document collection, regulatory monitoring, review routing, billing hygiene and reporting.

Modeled aviation-law workflow automation adoption, 2026:

Solo aviation lawyers: 20 percent

Small and SMB aviation firms: 28 percent

Mid-market aviation practices: 45 percent

AmLaw 200 and global aviation practices: 58 percent

In-house aviation legal departments: 48 percent

Overall aviation-law weighted estimate: 34 percent

Workflow automation adoption is strongest where there is enough matter volume to justify process design. Large firms and in-house teams have more incentive to automate because they manage larger contract portfolios, litigation dockets, regulatory calendars, discovery collections and outside counsel reporting.

The 2025 Legal Industry Report supports this direction of travel. It describes AI as increasingly useful beyond legal analysis, including billing, scheduling, correspondence, financial decision-making and practice operations. (American Bar Association) Clio’s 2025 reporting also found that growing law firms use automations such as consultation booking, document drafting and AI-assisted summarization more heavily than stable or shrinking firms. (2Civility)

In aviation law, the strongest workflow automation targets are:

- Regulatory update intake and routing

- FAA, DOT, TSA and EASA monitoring

- Aircraft lease review checklists

- Accident-response task lists

- Insurance coverage intake

- Passenger and cargo claim triage

- Discovery status tracking

- Matter-budget tracking

- Outside counsel invoice review

- Client reporting templates

The practical issue is that workflow automation requires more setup than generative AI. A lawyer can test a chatbot in five minutes. Building an aviation regulatory monitor, contract-review workflow or claims-triage process takes data cleanup, templates, permission rules and human review checkpoints.

AI legal research tools

AI legal research is the most mature category because lawyers already pay for legal research platforms and because aviation law is heavily dependent on statutes, regulations, agency guidance, administrative decisions, case law and prior interpretations.

Modeled aviation-law AI research adoption, 2026:

Solo aviation lawyers: 36 percent

Small and SMB aviation firms: 45 percent

Mid-market aviation practices: 62 percent

AmLaw 200 and global aviation practices: 78 percent

In-house aviation legal departments: 60 percent

Overall aviation-law weighted estimate: 49 percent

ABA technology reporting supports the idea that research is the most common AI-adjacent use case. A 2025 summary of the ABA Legal Technology Survey noted that legal research was the dominant application for AI tools, with 35 percent of respondents reporting use of legal analytics for legal research in the prior year. The same summary reported 23 percent using AI-related tools for case or matter strategy, 17 percent for understanding judges and 13 percent for predicting outcomes. (LawSites)

For aviation law, AI research adoption is especially compelling because the research universe is broad and layered. A lawyer may need to check FAA regulations, DOT enforcement materials, NTSB reports, TSA rules, airport grant assurances, EASA materials, ICAO standards, product-liability cases, federal preemption doctrine, Montreal Convention decisions, Warsaw Convention legacy cases, cargo-liability rules, state tort law and contract law.

That said, research AI cannot be treated as self-proving. ABA Formal Opinion 512 reminds lawyers that duties of competence, confidentiality, client communication and reasonable fees apply when using generative AI. The ABA specifically warns that lawyers must understand the benefits and risks of technology used to deliver legal services. (American Bar Association)

For aviation-law teams, that means AI research tools should be used with citation checking, source verification and jurisdictional review. A hallucinated aviation case or misread FAA rule is not just embarrassing. It can distort a safety-sensitive or high-value matter.

Predictive analytics adoption

Predictive analytics is the least mature major AI category in aviation law. The use cases are real, but adoption is slower because outcomes are hard to model and because aviation matters often involve unusual fact patterns, sparse datasets and high settlement confidentiality.

Modeled aviation-law predictive analytics adoption, 2026:

Solo aviation lawyers: 8 percent

Small and SMB aviation firms: 10 percent

Mid-market aviation practices: 18 percent

AmLaw 200 and global aviation practices: 30 percent

In-house aviation legal departments: 22 percent

Overall aviation-law weighted estimate: 14 percent

Predictive analytics is most useful in aviation law for:

- Venue and judge analysis

- Settlement range analysis

- Accident and injury claim valuation

- Cargo claim portfolio analysis

- Insurance exposure modeling

- Discovery burden forecasting

- Motion outcome research

- Opposing counsel behavior patterns

- Regulatory enforcement trend analysis

The ABA technology survey summary found that 13 percent of respondents used AI-related tools for predicting outcomes, which supports treating predictive analytics as real but still secondary to research, drafting and workflow automation. (LawSites)

For aviation law, predictive tools may work best when they are framed as decision-support rather than prediction. A tool that says “this claim will settle for X” is risky. A tool that shows historical ranges, judge tendencies, venue behavior, claim-type patterns and uncertainty bands is more credible.

Adoption by Firm Size

and global

legal departments

Tool Category Usage

Budget Allocation Trends

5. Workflow Decomposition Analysis

Aviation law is not one workflow. It is a bundle of workflows that behave very differently under automation pressure. Drafting a first-pass regulatory memo is not the same as negotiating an aircraft lease. Summarizing an accident record is not the same as making a privileged judgment call after a fatal incident. A good AI plan has to respect those differences.

The broader legal market is already moving toward workflow-level AI use rather than one-off experimentation. Thomson Reuters’ 2025 generative AI report frames GenAI as a technology that professionals expect to become embedded in everyday legal, tax, accounting, audit, risk, fraud and government workflows, not just used as a standalone writing tool. (Thomson Reuters) Clio’s 2025 Legal Trends reporting also ties firm growth to heavier use of AI and automation across common law-firm processes. (2Civility)

For aviation law, the practical question is this: where does AI safely remove friction, and where does it create new professional risk?

Workflow decomposition table

| Workflow | Time Allocation | AI Automation Potential | Risk if Automated Poorly | Cost Reduction Opportunity | Practical AI Role |

|---|---|---|---|---|---|

| Intake | 6% | 40% | Medium | 15% to 25% | Triage, conflict pre-checks, claim summaries and routing. |

| Research | 16% | 45% | High | 20% to 35% | Case law, FAA, DOT, NTSB and TSA materials, source summaries and research outlines. |

| Drafting | 22% | 42% | High | 18% to 32% | First drafts, issue lists, memos, pleadings, client alerts and matter summaries. |

| Negotiation | 8% | 22% | High | 8% to 15% | Clause comparison, fallback positions, issue trackers and negotiation prep. |

| Compliance | 13% | 38% | High | 15% to 28% | Obligation mapping, regulatory change summaries, checklists and gap analysis. |

| Litigation and Discovery | 15% | 32% | High | 12% to 25% | Chronologies, document review, deposition prep, privilege support and fact summaries. |

| Ongoing Monitoring | 7% | 50% | Medium | 20% to 40% | FAA, DOT, EASA and ICAO alerts, rule tracking, issue flagging and client updates. |

| Client Communication | 6% | 30% | Medium | 10% to 20% | Status updates, plain-English summaries, meeting prep and executive-ready briefings. |

| Billing and Administration | 7% | 39% | Low to Medium | 15% to 30% | Billing narratives, budget tracking, invoice review, staffing analysis and pricing support. |

Weighted automation potential: 38.4% of aviation-law billable or revenue-producing time

The 38.4 percent figure should not be read as “38.4 percent of lawyers go away.” That is the wrong interpretation. It means that roughly 38.4 percent of the work is exposed to meaningful compression, acceleration or redesign through AI-assisted workflows. In practice, only part of that exposed time turns into near-term savings because aviation-law work still requires lawyer review, citation checking, client judgment, privilege protection and risk management.

The ABA’s Formal Opinion 512 is important here because it makes clear that lawyers using generative AI remain bound by duties of competence, confidentiality, client communication and reasonable fees. In other words, AI can speed the work, but it does not move responsibility away from the lawyer. (American Bar Association)

Intake

Time allocation: 6%

AI automation potential: 40%

Risk exposure: Medium

Aviation intake is often more complex than standard legal intake because facts arrive in messy form. A passenger claim may include medical details, flight records, baggage information and treaty issues. An aircraft transaction may involve ownership, title, lien, registration, financing and export questions. An accident-related matter may raise privilege, preservation, insurance, regulatory and public-relations concerns almost immediately.

AI can help intake in four ways:

- Classify the matter type

- Extract key facts

- Identify missing information

- Route the matter to the right lawyer or team

For passenger, baggage, cargo and smaller insurance claims, AI can create immediate value by turning messy emails and attachments into a structured intake summary. For aircraft finance or regulatory matters, AI can prepare a preliminary checklist before a lawyer reviews the file.

The risk is over-triage. If the system incorrectly treats a serious safety, injury, sanctions, export-control or regulatory issue as routine, the firm can miss the moment when legal judgment matters most.

Recommended controls:

- Use AI for intake summaries, not final intake decisions

- Require human review for injury, accident, enforcement, sanctions and export-control triggers

- Build aviation-specific issue flags

- Keep privileged and confidential materials inside approved systems only

Research

Time allocation: 16%

AI automation potential: 45%

Risk exposure: High

Research is one of the clearest AI opportunities in aviation law because the source universe is wide. A single issue may involve federal regulations, agency guidance, enforcement materials, international treaties, state tort law, insurance law, contract law, accident reports and industry standards.

AI can help with:

- Initial research plans

- Case-law summaries

- Regulatory summaries

- Citation clustering

- Agency guidance comparison

- Treaty issue spotting

- Prior work-product retrieval

- Research memo outlines

Legal research is also one of the highest-risk categories because the output can sound authoritative even when it is wrong. ABA ethics guidance is directly relevant: lawyers must understand the benefits and risks of the technology they use and must protect client information while maintaining competence. (American Bar Association)

The best aviation-law research workflow is not “ask AI and paste the answer.” It is a controlled process:

- Ask AI to map the issue

- Force source-backed answers

- Verify primary authority

- Check jurisdiction and date

- Review agency materials directly

- Have a lawyer approve the final position

For aviation law, retrieval-augmented research is especially important. Tools should pull from trusted legal databases, FAA and DOT materials, NTSB documents, firm work product, contract templates and approved client files rather than relying on an unconstrained model.

Drafting

Time allocation: 22%

AI automation potential: 42%

Risk exposure: High

Drafting is the largest workflow category in the model. It includes client memos, regulatory updates, pleadings, motions, discovery requests, settlement letters, aviation contract markups, demand packages, board updates, internal investigation summaries and first-pass legal analysis.

The 2025 Legal Industry Report found that AI is already being used for drafting correspondence and related operational work, which supports treating drafting as one of the first legal tasks to absorb AI assistance. (American Bar Association) In aviation law, the most useful drafting applications are not flashy. They are practical:

- Turn notes into a clean memo structure

- Draft client alerts from regulatory updates

- Generate first-pass chronologies

- Summarize claims files

- Build issue lists from aircraft contracts

- Prepare privilege-log descriptions

- Draft routine discovery correspondence

- Convert legal analysis into executive summaries

The cost reduction opportunity is meaningful because many drafting tasks begin with a blank-page problem. AI reduces that friction. But the lawyer still needs to own the final document.

The highest-risk drafting areas are pleadings, motions, regulatory submissions and client advice that cites legal authority. The Mata v. Avianca sanctions episode remains the cautionary tale for lawyers using generative AI without proper citation verification. ABA Formal Opinion 512 was issued in the wake of exactly these concerns about competence, confidentiality and accuracy. (American Bar Association)

Recommended controls:

- No AI-generated legal citation should be used without source verification

- Create approved aviation-law prompt and template libraries

- Separate low-risk drafting from legal-advice drafting

- Require senior review for accident, safety, enforcement and litigation filings

- Track whether AI reduced time so pricing can be adjusted honestly

Negotiation

Time allocation: 8%

AI automation potential: 22%

Risk exposure: High

Negotiation is less automatable than research or drafting because it depends on leverage, context, personalities, business objectives and timing. In aircraft leasing, maintenance contracts, airport-use agreements or insurance settlements, the legal words matter, but so do commercial pressure, risk appetite and deal history.

AI can still help. It can prepare lawyers by:

- Comparing clause versions

- Identifying deviations from precedent

- Summarizing counterparty positions

- Suggesting fallback language

- Creating negotiation trackers

- Preparing risk-ranked issue lists

- Summarizing prior deal positions

The AI opportunity is not to negotiate for the lawyer. It is to make the lawyer better prepared before the negotiation starts.

Risk is high because a model may suggest language that is commercially unrealistic or legally inappropriate. In aviation transactions, a small change to indemnity, maintenance obligations, return conditions, insurance requirements, export compliance, governing law or default remedies can shift millions of dollars of risk.

Best use case:

AI prepares the map. Lawyers decide the route.

Compliance

Time allocation: 13%

AI automation potential: 38%

Risk exposure: High

Compliance is one of the most attractive workflow categories for aviation AI because aviation is rule-heavy and constantly changing. FAA, DOT, TSA, EASA, ICAO, sanctions, export controls, airport rules, safety requirements, passenger-protection obligations and drone regulations all create monitoring burdens.

AI can support:

- Regulatory change detection

- Obligation mapping

- Policy comparison

- Compliance checklist generation

- Internal training summaries

- Enforcement trend summaries

- Audit preparation

- Gap analysis across jurisdictions

The legal AI market’s growth is closely tied to use cases such as regulatory compliance, contract review, eDiscovery and case prediction, according to Grand View Research’s legal AI market analysis. That aligns well with aviation law because compliance monitoring is a natural AI workflow when paired with trusted sources and legal review. (Thomson Reuters)

The risk is false confidence. A compliance monitor that misses an FAA rule change, a DOT passenger-protection development, a TSA security update or an EASA requirement can create real exposure. For that reason, compliance AI should be designed as a monitoring and escalation system, not a final legal authority.

Practical structure:

- AI monitors source feeds

- AI flags possible changes

- A lawyer validates relevance

- The firm or legal department updates the obligation library

- The client receives a plain-English action summary

Litigation and discovery

Time allocation: 15%

AI automation potential: 32%

Risk exposure: High

Aviation litigation is built on facts. Accident records, maintenance logs, flight data, crew communications, weather records, medical records, passenger files, cargo documents, insurance materials, expert reports and regulatory correspondence can create huge document volumes.

AI is already familiar in litigation through technology-assisted review and eDiscovery. ABA Formal Opinion 512 notes that AI-based technologies have long been used in eDiscovery to categorize documents as responsive or non-responsive and to segregate privileged documents. (LawSites)

In aviation litigation, AI can help with:

- Document classification

- Chronology building

- Witness file summaries

- Deposition preparation

- Expert-material organization

- Privilege review support

- Issue tagging

- Medical and damages summaries

- Settlement packet drafting

- Motion record assembly

The risk is not simply hallucination. It is missed nuance. Aviation litigation often turns on technical facts: maintenance history, component failure, crew decision-making, airworthiness directives, weather, training, manuals, warnings, causation and regulatory context. AI can organize these facts, but lawyers and experts must interpret them.

High-value AI use case:

Build a live aviation matter chronology that links each key fact to source documents, deposition testimony, regulatory materials and expert issues.

Low-value or risky AI use case:

Ask a model to “predict liability” without structured facts, expert context or jurisdiction-specific law.

Ongoing monitoring

Time allocation: 7%

AI automation potential: 50%

Risk exposure: Medium

Ongoing monitoring is one of the best early AI workflows because the task is repetitive, bounded and source-driven. Aviation clients often need to know when an agency changes a rule, opens a consultation, issues enforcement guidance, releases safety information, changes certification expectations or updates passenger-protection requirements.

AI can monitor:

- FAA rulemaking and guidance

- DOT aviation consumer protection developments

- TSA security updates

- NTSB reports and recommendations

- EASA and ICAO materials

- State airport and aviation rules

- Drone and AAM developments

- Sanctions and export-control changes affecting aviation assets

This workflow should be built like a newsroom plus a legal desk. AI finds and summarizes changes. A lawyer decides whether the change matters, what the client should do and how urgent the issue is.

Cost reduction can be strong because monitoring is recurring. The client value is also obvious: fewer missed updates, faster alerts and better targeting by issue type.

Client communication

Time allocation: 6%

AI automation potential: 30%

Risk exposure: Medium

Client communication is not just email. It includes matter updates, budget explanations, legal risk summaries, board-ready briefings, claim status reports, regulatory change alerts and plain-English explanations for non-lawyer stakeholders.

AI can help turn dense legal work into usable communication. That matters in aviation because the client audience is often mixed: legal, operations, safety, finance, insurance, compliance and executive teams.

Useful AI tasks include:

- Drafting status updates

- Creating executive summaries

- Converting legal analysis into operational next steps

- Preparing meeting agendas

- Summarizing open issues

- Translating legalese into business language

- Producing client-facing dashboards

The risk is tone and overstatement. A model may write confidently about a legal position that is still uncertain. It may also remove caveats that matter. Lawyers should treat AI communication drafts as a starting point, not a client-ready product.

Thomson Reuters’ 2025 report emphasizes that GenAI adoption is moving into professional workflows, but the legal profession still has to manage quality, risk and judgment. That is exactly the balance needed for client communication. (Thomson Reuters)

Billing, pricing and matter administration

Time allocation: 7%

AI automation potential: 39%

Risk exposure: Low to medium

Billing and administration are not glamorous, but they are economically important. AI can improve:

- Billing narratives

- Time entry cleanup

- Matter budget tracking

- Invoice review

- Alternative-fee modeling

- Phase-code analysis

- Staffing analysis

- Realization tracking

- Client reporting

This is one of the safest early workflows because it rarely asks AI to make final legal judgments. It also connects directly to client pressure. If AI reduces time spent on routine tasks, clients will expect greater pricing transparency.

ABA Formal Opinion 512 also flags fees as part of the ethical analysis for lawyers using generative AI. That matters because firms cannot simply charge the same way forever if AI materially changes the time required for certain tasks. (American Bar Association)

Aviation-law firms should use AI billing analytics to answer three questions:

Which tasks are shrinking?

Which tasks still require senior legal judgment?

Where should pricing move from hourly to fixed, capped or subscription models?

Billable Hours vs Automation Potential

Time Savings Model (before vs after AI)

6. Revenue Model Sensitivity Analysis

AI does not hit every aviation-law revenue model the same way. That is the whole point of this section.

A firm billing by the hour may feel AI as revenue pressure. A firm using flat fees may feel it as margin expansion. A contingency practice may feel it as better case selection and lower cost per file. An in-house legal department may feel it as reduced outside counsel demand. The same productivity gain can look like a threat, a profit lever or a client-retention tool depending on how the work is priced.

This matters because the legal market is already moving toward pricing pressure. Clio’s 2025 Legal Trends reporting noted that firms may need to move away from hourly billing toward more flexible fee models as AI reduces time spent on billable work. The same reporting said 59 percent of firms used flat fees either exclusively or alongside hourly billing in 2024, and that 45 percent of firms using AI widely had adjusted pricing as a result. (2Civility)

The ethics overlay is just as important as the economics. ABA Formal Opinion 512 says lawyers using generative AI remain responsible for competence, confidentiality, communication and reasonable fees. That means AI-created efficiency cannot simply be hidden inside an old billing model forever, especially where the client is being charged for time. (American Bar Association, LawSites)

Hourly billing exposure

Hourly billing is the most exposed model because revenue is directly tied to time.

Before AI:

1,000 hours × $600/hour = $600,000

After AI:

923 hours × $600/hour = $553,800

Revenue impact:

$46,200 revenue reduction

7.7 percent revenue compression

This is the cleanest version of the threat. If the firm bills strictly by hours worked and passes all time savings through to the client, revenue falls. The work may be done faster, but the firm captures none of the productivity upside unless it replaces the lost hours with new work.

Hourly billing is not dead. It will still make sense for high-uncertainty work: accident response, regulatory investigations, high-stakes litigation, novel FAA or DOT issues, complex aircraft finance negotiations and cross-border matters where scope is unpredictable. But routine research, first drafts, contract markups, matter updates and monitoring are harder to defend as open-ended hourly work once AI reduces the time required.

Clio’s 2025 reporting makes this point directly: as AI reduces time spent on billable work, firms relying heavily on hourly billing may see revenue pressure unless they rethink pricing. (Clio, 2Civility)

Flat-fee scalability

Flat-fee work flips the economics.

If a firm charges a fixed $600,000 fee for the same matter and AI reduces delivery time from 1,000 hours to 923 hours, revenue stays flat while cost falls.

Before AI:

Revenue: $600,000

Delivery cost: 1,000 hours × $225/hour = $225,000

Gross margin: $375,000

Gross margin percentage: 62.5 percent

After AI:

Revenue: $600,000

Delivery cost: 923 hours × $225/hour = $207,675

Gross margin: $392,325

Gross margin percentage: 65.4 percent

Margin impact:

Incremental margin gain: $17,325

Margin expansion: 2.9 percentage points

This is why flat fees are so attractive in AI-exposed workflows. The client gets price certainty. The firm gets upside from operational efficiency. The risk is scope control. A flat fee only works if the firm understands the workflow well enough to price it.

Good aviation-law candidates for flat-fee AI-enhanced delivery:

- Aircraft purchase agreement review

- Aircraft lease issue spotting

- FAA registration support

- Drone compliance starter packages

- Routine regulatory-update memos

- Cargo claim demand packages

- Passenger claim triage

- Outside counsel matter summaries

- Aviation insurance policy review

- Recurring contract playbook updates

Contingency-fee exposure

Contingency practices are less exposed to direct revenue compression because fees are usually tied to recovery, not hours. AI does not automatically reduce the fee if the lawyer spends fewer hours.

That does not mean contingency practices are untouched. AI changes the cost curve.

In plaintiff-side aviation injury, passenger claims, cargo loss, insurance disputes and certain commercial aviation claims, AI can help with:

- Case intake

- Claim scoring

- Medical record summaries

- Liability fact timelines

- Demand package drafting

- Settlement range research

- Document organization

- Client updates

- Litigation budget forecasting

The main economic effect is lower cost per case and better case selection. A contingency firm that reduces drafting and file-review time can handle more matters with the same staff, or it can focus staff time on higher-value cases.

Example contingency model:

Expected recovery: $900,000

Contingency fee: 33 percent

Gross fee: $297,000

Internal hours before AI: 420

Internal cost at $225/hour: $94,500

Internal hours after AI, with 12 percent overall compression: 370

Internal cost after AI: $83,250

Margin improvement: $11,250 per matter

The client-facing fee may not change. The firm’s risk-adjusted economics improve.

The main caution is quality control. Aviation claims can turn on technical facts, causation, medical evidence, treaty limits, jurisdiction, product issues, weather, maintenance, passenger conduct or carrier defenses. AI can support triage, but it should not make the final go/no-go decision alone.

Subscription legal model viability

Subscription legal models are still early in aviation law, but AI makes them more viable.

The model works best where the client needs recurring, bounded support but not constant bespoke advice. That describes many smaller aviation businesses.

Good candidates:

- Drone operators

- Charter operators

- Aircraft management companies

- Maintenance providers

- Airport vendors

- Small cargo operators

- Aviation startups

- Private aircraft ownership groups

- Regional aviation service businesses

Subscription packages might include:

- Monthly regulatory updates

- FAA/DOT monitoring

- Template reviews

- Policy refreshes

- Short legal Q&A windows

- Contract issue spotting

- Compliance checklist maintenance

- Quarterly legal risk reviews

AI improves the economics because the firm can monitor more issues, summarize more sources and produce more repeatable client-facing materials without starting from scratch every month.

Illustrative subscription model:

50 aviation clients

Monthly fee: $2,500

Annual recurring revenue: $1.5 million

Monthly legal operations hours before AI: 12 hours per client

Monthly legal operations hours after AI: 8 hours per client

Monthly hours saved: 200

Annual hours saved: 2,400

At $225 loaded cost per hour, annual delivery-cost savings equal $540,000.

This model only works if the scope is clear. Subscription legal services should not create an expectation of unlimited accident response, litigation, enforcement defense or major transaction support. Those should remain separately scoped.

Revenue Compression Model

Margin Expansion Model

7. Competitive AI Vendor Landscape

The AI vendor market for aviation law is crowded, but not yet aviation-specific.

That is the big takeaway. Most vendors selling into this space today are horizontal legal AI platforms, legal research tools, contract AI systems, eDiscovery platforms, intake tools or compliance-monitoring products. They can serve aviation-law workflows, but very few are built specifically for FAA, DOT, TSA, NTSB, EASA, ICAO, aircraft leasing, aviation insurance, drone regulation, airport operations or accident-response work.

That gap is the opening.

The legal AI market is now moving from “interesting tool” to “infrastructure layer.” Harvey announced a $200 million raise at an $11 billion valuation in March 2026, while Legora announced a $150 million Series C at a $1.8 billion valuation in October 2025. Those two companies alone show how much capital is chasing the legal AI platform layer. (Harvey, Legora)

At the same time, incumbents are not standing still. Thomson Reuters acquired Casetext for $650 million in cash in 2023, giving it CoCounsel, one of the first major GPT-4 legal assistants. LexisNexis launched Lexis+ AI as a secure generative AI legal platform with linked legal citations, and vLex’s Vincent AI is now positioned as an AI legal workflow platform backed by vLex’s global legal database. (Thomson Reuters, LexisNexis, vLex)

For aviation law, this creates a split market:

- General legal AI platforms will win broad enterprise access.

- Legal research incumbents will remain trusted for authority-backed research.

- Contract AI vendors will win aircraft leasing, purchase, MRO and vendor-agreement workflows.

- eDiscovery and litigation AI vendors will win accident, product-liability and insurance disputes.

- Compliance-monitoring tools will win recurring FAA, DOT, TSA, EASA, ICAO and drone-law updates.

- Vertical aviation-law tools remain mostly white space.

Vendor landscape by category

| Vendor | Category | Funding / Valuation Signal | Estimated ARR Visibility | Primary Customer Segment | Differentiation for Aviation Law |

|---|---|---|---|---|---|

| Harvey | Legal AI platform | $200M raise at $11B valuation in 2026. Source | Earlier public reporting described around $100M ARR and 500+ customers. Current ARR not fully disclosed. | AmLaw firms, global firms, large in-house teams. | Enterprise-grade assistant for research, document review, drafting, contract analysis and large-scale knowledge work. |

| Legora | Collaborative legal AI | $150M Series C at $1.8B valuation in 2025. Source | Current ARR not disclosed. Earlier third-party reports placed recurring revenue in the low eight-figure range. | Large firms, international firms, enterprise legal teams. | Strong collaboration layer, attorney workflow design and global-firm adoption momentum. |

| CoCounsel / Thomson Reuters | AI legal research | Thomson Reuters acquired Casetext for $650M cash in 2023. Source | Not disclosed separately after acquisition. | Law firms, corporate legal teams, government. | Trusted content stack, Westlaw and Practical Law ecosystem, strong fit for research-heavy aviation workflows. |

| Lexis+ AI | Research and drafting | Product of LexisNexis. No venture funding metric applicable. | Not separately disclosed. | Law firms, legal departments, research-intensive users. | Linked citations, Shepard’s integration and authoritative legal content for citation-sensitive aviation work. |

| vLex Vincent AI / Clio | Global legal research | vLex launched Vincent AI in 2024; Clio/vLex transaction positioned vLex as a global legal AI platform. Source | Not separately disclosed. | Firms needing global and comparative legal research. | Strong international content footprint for cross-border aviation, leasing, treaty and regulatory issues. |

| Spellbook | Contract AI | $50M Series B at $350M valuation in 2025. Source | Not disclosed. LAW.co modeled range: $10M to $30M. | SMB firms, boutiques, transactional teams. | Practical contract drafting and review inside lawyer workflows, useful for aviation contracts and owner-operator work. |

| Ironclad | CLM and AI contracting | Reported prior funding totaled roughly $333M with a $3.2B valuation in third-party profiles. | Reported surpassing $200M ARR in 2026. Source | Enterprise legal, procurement, sales and commercial teams. | Strong fit for high-volume aviation vendor contracts, MRO agreements, airport vendor agreements and procurement workflows. |

| LegalOn | Contract review AI | $50M Series E led by Goldman Sachs; $200M total funding. Source | Not disclosed. LAW.co modeled range: $25M to $75M. | In-house legal, contract teams, global enterprises. | Contract review with legal playbooks and matter-management orientation. |

| Luminance | Diligence and contract analysis | $75M Series C; more than $115M raised over the prior 12 months. Source | Not disclosed. LAW.co modeled range: $15M to $50M. | Enterprise legal, law firms, diligence-heavy teams. | Strong due diligence and contract-analysis posture, useful for aircraft portfolio review and lease abstraction. |

| Robin AI | Contract copilot | $26M Series B led by Temasek in 2024, plus later customer-led funding. Source | Not disclosed. LAW.co modeled range: $10M to $30M. | Enterprise legal and business contracting teams. | Human-in-the-loop contracting and reports, useful for repeat aviation commercial agreements. |

| Evisort / Workday | Document intelligence | Workday signed a definitive agreement to acquire Evisort in 2024. Source | Not disclosed. One analyst estimate put revenue run rate near $30M before acquisition. | Enterprise legal, finance, HR and procurement. | Enterprise-document intelligence, useful where aviation contracts connect to finance and operations systems. |

| Relativity | eDiscovery and investigations | Third-party estimates place Relativity around a $3.6B valuation. Treat as directional, not company-reported. | Third-party estimate: $200M+ ARR. Source | Litigation teams, enterprises, government and investigations. | Strong for accident litigation, product-liability discovery, regulatory investigations and aviation insurance disputes. |

| Eve | Plaintiff-law AI | $103M Series B at over $1B valuation in 2025. Source | Not disclosed. LAW.co modeled range: $15M to $50M. | Plaintiff-side firms. | Useful analogue for aviation passenger injury, claimant-side accident workflows and high-volume claim operations. |

| Supio | PI and mass-tort AI | $60M Series B in 2025; $91M total funding. Source | Not disclosed. LAW.co modeled range: $10M to $35M. | PI, mass tort and plaintiff firms. | Human-verified document analysis model could translate to aviation injury and mass-claim workflows. |

| Theo Ai | Litigation prediction | $4.2M seed round in 2025 after earlier pre-seed funding. Source | Early stage. ARR not disclosed. | Big Law, litigation funders, enterprises. | Settlement prediction and litigation analytics, relevant to aviation claims but requiring careful validation. |

Vendor Funding Timeline

Market Share Estimate

AI Vendor Positioning Matrix (Enterprise vs SMB)

8. Appendix

Core data source catalog

| Data Category | Primary Source | Use in Report | Notes | Confidence |

|---|---|---|---|---|

| U.S. lawyer population | ABA Profile of the Legal Profession / National Lawyer Population Survey Source | Used as the broad denominator for legal-market sizing and niche-share modeling. | ABA reported that the U.S. lawyer population rose to 1.37 million in 2025 from 1.35 million in 2024. | High |