Intelligence in Intellectual Property (IP) Market Research Report

The category is already real. The open question is not whether AI will matter. It is whether firms will use it to protect margin and improve client value, or watch clients use it to pull work in-house.

1. Executive Summary

Definition of the sub-category

Artificial Intelligence for IP sits at the intersection of three large pools of spend: global IP legal services, legal AI software, and the broader knowledge work of invention disclosure, patent prosecution, portfolio management, licensing, enforcement, and brand protection.

The category is already real. The open question is not whether AI will matter. It is whether firms will use it to protect margin and improve client value, or watch clients use it to pull work in-house.

Market size (U.S. + global)

The global IP law firm services market was estimated at $14.98 billion in 2024 and projected to reach $46.05 billion by 2032. The global legal AI market was much smaller at $1.45 billion in 2024, but it is growing faster and is projected to reach $3.90 billion by 2030. Those numbers create the basic market tension: AI software is still a small spend category compared with the legal work it can influence.

For the U.S., IP legal services revenue is modeled at roughly $6.0 billion in 2024, equal to about 40% of the cited global IP law firm services market. That estimate is intentionally conservative for high-value U.S. patent, trademark, copyright, trade-secret, licensing, and litigation work. It should be treated as a planning range, not a census.

Estimated current AI penetration (% of firms using AI)

Current AI penetration is uneven. Thomson Reuters reported that 26% of legal professionals already used GenAI in early 2025, with 28% adoption among law firms and 23% among corporate legal departments. A separate ABA survey summary found 30% of private-practice respondents using AI technology in 2024, including 46% among firms with 100 or more attorneys and 18% among solos. In-house legal adoption is moving faster now: the ACC and Everlaw reported 52% of in-house counsel actively using GenAI in 2025.

Core disruption vectors

| Vector | What changes | Current maturity | Economic bite |

|---|---|---|---|

| Research compression | Prior art, case law, claim construction, freedom-to-operate, invalidity searches, and litigation research move from hours of manual hunting toward AI-assisted synthesis. | High for assisted research | Cuts low-leverage research time and raises client pressure for fixed or capped fees. |

| Drafting automation | Patent application sections, office-action responses, trademark responses, licensing terms, claim charts, cease-and-desist drafts, and portfolio summaries start from structured AI drafts. | Medium to high | Drafting-heavy revenue becomes exposed under hourly billing but margin improves under flat fees. |

| Portfolio intelligence | AI connects patents, products, competitors, maintenance fees, licensing targets, claim strength, and litigation risk. | Medium | Turns IP from a filing function into a business intelligence function. |

| Enforcement and monitoring | AI watches marketplaces, app stores, product releases, code repositories, advertising, and global filing activity. | Medium | More matters are found earlier, but clients expect lower monitoring costs. |

| Pricing transparency | Clients ask what AI did, where time was saved, and why the bill did not change. | Early but rising | Changes procurement conversations even when the legal doctrine stays the same. |

Estimated automation potential (% of billable time)

Estimated automation potential across IP billable time: 32% to 55% depending on workflow, with a blended planning estimate of 39% for tasks that can be materially accelerated but still require attorney review. This is directionally consistent with broader labor-market estimates that legal work has unusually high exposure to AI-assisted automation, but this report uses a narrower IP workflow model because patent and litigation work include high-risk judgment, strategy, and client counseling that should not be automated away.

5-year outlook

By 2030, legal AI will likely be a normal part of IP practice management, not a novelty. The winners will not be firms that replace lawyers. They will be firms that redesign work intake, drafting, supervision, portfolio analytics, and pricing around a faster production engine.

Strategic risks if firms ignore AI

Strategic risk if firms ignore AI: clients may not leave immediately, but they will ask sharper questions. In-house teams already expect GenAI to reduce reliance on outside counsel, and 61% of surveyed in-house counsel said they are likely to push for pricing changes in outside legal services.

Market Size Snapshot

AI Adoption Curve

Revenue vs Automation Exposure

2. Definition and Market Scope

Artificial Intelligence for Intellectual Property means AI tools and AI-enabled workflows used to create, protect, manage, license, enforce, value, and defend intellectual property.

Put more simply, this is not just “AI for lawyers.” It is AI applied to patents, trademarks, copyrights, trade secrets, IP litigation, licensing, portfolio strategy, and brand protection.

A general chatbot used to summarize a meeting is not necessarily IP AI. But a system that helps draft an office-action response, compare patent claims against prior art, monitor counterfeit listings, flag trademark conflicts, or summarize a patent portfolio for a licensing review fits squarely inside the category.

What is in scope

The market includes AI used across the full IP lifecycle:

Invention intake and patentability screening, where AI helps turn raw technical disclosures into structured summaries, early prior art searches, and prosecution-ready materials.

Patent prosecution, including prior art review, claim drafting support, office-action analysis, IDS review, patent family mapping, and portfolio maintenance decisions.

Trademark and brand protection, including clearance searches, similarity analysis, marketplace monitoring, takedown triage, and draft responses to office actions.

Copyright and digital media work, including infringement detection, licensing support, DMCA workflows, chain-of-title review, and content ownership analysis.

Trade secret protection, including risk classification, access monitoring, employee-exit review, policy compliance, and evidence preservation.

IP litigation, including claim charts, invalidity contentions, discovery review, expert-report support, damages research, and settlement analysis.

Licensing and transactions, including contract review, royalty benchmarking, diligence summaries, clause comparison, and portfolio valuation.

Portfolio management, including maintenance-fee decisions, competitor tracking, whitespace analysis, pruning recommendations, and business-unit reporting.

The global IP law firm services market was valued at $14.98 billion in 2024 and projected to reach $46.05 billion by 2032, according to Verified Market Research. That gives the category a useful global revenue anchor, even though the real AI opportunity is broader than law firm revenue alone because in-house teams, legal tech vendors, and managed-service providers also participate in the workflow. (Verified Market Research)

For U.S. context, IBISWorld places the broader U.S. law firms market at $426.7 billion in 2025. IP law is only a slice of that market, but it is a high-value slice because it is tied to technology, brands, litigation risk, corporate transactions, and intangible-asset strategy. (IBISWorld)

Who buys and uses IP AI

The market is split across several buyer groups, and each one feels AI pressure differently.

Solo lawyers and small firms tend to use AI for speed. For them, the value is faster intake, cleaner first drafts, lower research burden, and the ability to offer flat-fee services without crushing margins.

Boutique IP firms are one of the most exposed segments. Patent prosecution, trademark portfolios, prior art review, office actions, and monitoring all contain repeatable work that AI can speed up. These firms are not necessarily at risk because they are small. Many boutiques are technically excellent. The risk is that clients will expect better speed, cleaner reporting, and more transparent pricing.

Mid-market firms face a different kind of pressure. They often handle regional IP litigation, licensing, commercial disputes, and portfolio support. AI can reduce research and document-heavy work, which means these firms need to protect margin through better matter design, not just more hours.

AmLaw and large firms sit at the premium end of the market. Their highest-value work, such as major IP litigation, global licensing, M&A diligence, and bet-the-company portfolio strategy, will still require senior judgment. But clients will still ask the obvious question: if AI made the work faster, why did the bill stay the same?

In-house legal departments may be the most important buyers over the next five years. They are under budget pressure, and AI gives them a way to pull routine research, first-draft work, portfolio reporting, and outside-counsel supervision back inside.

ALSPs and legal tech providers are the wild card. They can use AI to industrialize work that law firms have historically billed by the hour, especially monitoring, review, data cleanup, docket hygiene, portfolio analysis, and repeatable reporting.

Attorney population

The cleanest public count for the patent side of the IP market comes from the USPTO’s Office of Enrollment and Discipline roster. The USPTO roster lists 53,710 active patent practitioners, including 38,307 patent attorneys and 14,488 patent agents. These are people authorized to practice before the USPTO in patent matters. (USPTO)

That number is useful, but it is not the whole IP bar. The USPTO patent-practitioner roster does not capture many trademark lawyers, copyright lawyers, trade-secret lawyers, licensing lawyers, or IP litigators who do not prosecute patents.

For broader legal-market context, the ABA reported 1.37 million active lawyers in the United States in 2025. Patent attorneys on the USPTO roster therefore represent roughly 2.8% of all U.S. lawyers before adding the non-patent IP lawyers who sit outside the patent roster. (American Bar Association)

A practical planning estimate for the broader U.S. IP attorney universe is about 60,000 to 70,000 lawyers. That estimate starts with registered patent attorneys, then adds attorneys focused on trademarks, copyright, trade secrets, licensing, and IP litigation. It should be treated as a modeled range, not an official census, because no single public dataset captures the entire IP legal workforce across all sub-practices.

Revenue model

AI does not hit every revenue model the same way.

Hourly work is the most exposed. Litigation research, claim-chart work, prior art analysis, diligence, opinion letters, and complex drafting can all take fewer hours with AI support. That creates revenue compression if the firm’s only pricing logic is “hours times rate.”

Fixed-fee work is different. In patent prosecution, trademark filings, portfolio cleanup, and standardized licensing support, AI can expand margins if the firm keeps pricing stable while reducing production time.

Subscription models may become more attractive. Brand monitoring, portfolio reporting, startup IP counseling, competitive tracking, and outside-counsel dashboards are natural candidates for recurring service packages.

Contingency and success-fee work is less about hour reduction and more about case selection. AI can help screen enforcement opportunities, estimate litigation risk, organize evidence, and decide which matters deserve investment.

Hybrid and alternative-fee arrangements may become the default for sophisticated clients. The more clients understand that AI can reduce time, the more they will push firms to price based on value, speed, and outcomes rather than raw labor.

Geography

IP work clusters around technology, life sciences, entertainment, brands, manufacturing, venture capital, federal courts, and corporate headquarters.

The most important U.S. markets include California for software, semiconductors, AI, venture-backed companies, platforms, and entertainment; New York for media, fashion, brands, finance, licensing, and litigation; Washington, D.C. and Northern Virginia for USPTO access, Federal Circuit work, policy, and government-facing IP matters; Texas for patent litigation, technology, energy, and enterprise software; Massachusetts for biotech, universities, robotics, and deep tech; Illinois for national law firms, manufacturing, brands, and litigation; and Washington state for cloud, e-commerce, gaming, and enterprise technology.

The patent bar is somewhat more portable than many local legal markets because patent practice before the USPTO is federally credentialed. The USPTO notes that only registered patent attorneys, registered patent agents, and individuals with limited recognition may represent others before the USPTO in patent matters. (USPTO)

Baseline market-sizing assumptions

For modeling purposes, this section uses the following anchors:

Global IP law firm services market: $14.98 billion in 2024, with a projected $46.05 billion by 2032. Source: (Verified Market Research)

U.S. law firms market: $426.7 billion in 2025. Source: (IBISWorld)

Active U.S. patent practitioners: 53,710. Source: (USPTO)

Active U.S. patent attorneys: 38,307. Source: (USPTO

Active U.S. lawyers: 1.37 million in 2025. Source: (American Bar Association)

Modeled U.S. IP legal services revenue: about $6.0 billion. This is a planning estimate based on the U.S. share of global IP law firm services.

Modeled broader U.S. IP attorney population: about 60,000 to 70,000 attorneys. This is a planning estimate that expands beyond the USPTO patent roster to include trademark, copyright, trade-secret, licensing, and litigation lawyers.

Firm Size Distribution

Revenue Breakdown by Firm Tier

Geographic Concentration Heat Map

3. Total Addressable Market: TAM, SAM, SOM

The market opportunity for AI in Intellectual Property can be measured two ways.

First, there is the legal-services revenue pool: the money clients already spend on IP legal work. This is the pool AI can compress, reshape, or help firms deliver more profitably.

Second, there is the AI software and services spend pool: the money firms, in-house teams, and legal operations groups will pay to buy tools that improve IP workflows.

Both matter. The first tells us where the disruption sits. The second tells us where vendors can earn revenue.

Market sizing headline

The core U.S. AI-for-IP model uses a $6.0 billion modeled U.S. IP legal services revenue pool. That estimate is based on the global IP law firm services market, which Verified Market Research valued at $14.98 billion in 2024 and projected to reach $46.05 billion by 2032. (Verified Market Research)

The legal AI market is much smaller today, but it is growing faster. Grand View Research estimated the global legal AI market at $1.45 billion in 2024 and projected it to reach $3.90 billion by 2030, a 17.3% CAGR from 2025 to 2030. North America accounted for more than 46% of global legal AI revenue in 2024. (Grand View Research)

That gap is the opportunity. AI software spend is still tiny compared with the legal work it can affect.

TAM: Total Addressable Market

TAM represents the full legal-services revenue pool that AI could influence in the IP market.

For the U.S. model:

TAM = modeled U.S. IP legal services revenue

TAM = $6.0 billion

For the global model:

TAM = global IP law firm services market

TAM = $14.98 billion in 2024

This does not mean AI vendors can capture $6.0 billion in the U.S. today. It means $6.0 billion of U.S. IP legal work is exposed to AI-enabled workflow redesign, pricing pressure, margin expansion, or service substitution.

The market is especially attractive because the work is document-heavy, research-heavy, and repeatable in places. Patent prosecution, trademark clearance, office-action response drafting, prior art review, claim charts, monitoring, portfolio reporting, and licensing review all create structured tasks that AI can speed up.

SAM: Serviceable Addressable Market

SAM narrows TAM to the portion of IP legal work that AI can realistically affect.

For this model, the blended automation-exposure assumption is 39% of U.S. IP billable-work value. That does not mean 39% of lawyers disappear. It means roughly 39% of the work value is tied to tasks AI can materially accelerate, restructure, or partially automate with human review.

SAM formula:

SAM = TAM × AI-addressable workflow share

SAM = $6.0B × 39%

SAM = $2.34B

So the modeled U.S. SAM for AI-addressable IP legal work is about $2.34 billion.

For global context:

Global SAM = $14.98B × 39%

Global SAM = about $5.84B

This is a practical planning number. It includes work where AI can touch the production engine, not every dollar of strategic counseling, litigation judgment, negotiation leverage, or client relationship value.

SOM: Serviceable Obtainable Market

SOM estimates what AI vendors and AI-enabled service providers could realistically capture over time.

There are two useful SOM views.

The first is a software spend view. If U.S. IP-focused firms, in-house teams, and service providers convert 8% to 15% of the $2.34 billion AI-addressable workflow pool into software, data, workflow automation, and managed AI services, the near-to-midterm U.S. SOM would be:

Low case: $2.34B × 8% = $187M

Base case: $2.34B × 12% = $281M

High case: $2.34B × 15% = $351M

The second is an AI-enabled services view. If firms and ALSPs use AI to repackage work into flat-fee, subscription, portfolio-monitoring, and managed-service offerings, the obtainable revenue pool is larger because the provider is not just selling software. It is selling a new delivery model.

For AI-enabled IP services, a practical 5-to-10-year U.S. SOM range is:

Conservative case: $500M

Base case: $900M

Aggressive case: $1.4B

The aggressive case assumes faster in-house adoption, stronger client pressure on outside counsel pricing, and rapid bundling of AI into IP portfolio operations.

Why SAM is not the same as “automation”

The word “automation” can be misleading in legal services. In IP, very little valuable work should be fully automated without review. A patent claim, trademark refusal response, invalidity argument, licensing position, or litigation strategy can create real liability if handled carelessly.

The better frame is acceleration.

AI can accelerate the work by reducing first-draft time, finding relevant materials faster, spotting patterns across portfolios, surfacing risks, creating comparison tables, and generating client-ready summaries. But attorneys still need to review, revise, sign off, and own the strategy.

That is why this model uses AI-addressable workflow value, not full labor replacement.

Legal tech spending logic

The legal AI market is still early. Grand View Research places the global legal AI market at $1.45 billion in 2024, while the global IP law firm services market is more than ten times larger at $14.98 billion. (Grand View Research, Verified Market Research)

That ratio matters. If AI becomes a standard operating layer inside IP law, even small shifts in budget allocation can create a sizable vendor market.

A boutique IP firm spending 1% to 2% of revenue on AI tools may start with research, drafting, docket intelligence, and client reporting.

A large firm may spend more in absolute dollars, but deployment is slower because procurement, security, training, and risk controls are heavier.

An in-house legal department may spend aggressively if AI helps reduce outside counsel reliance, improve portfolio visibility, or support faster business decisions.

ALSPs and legal ops providers may spend the highest share of revenue on AI because their business model depends on process efficiency.

TAM vs SAM vs SOM

AI Spend Growth Forecast (5–10 year CAGR)

AI Budget Allocation by Firm Size

4. Current State of AI Adoption

AI adoption in legal services has moved past the “curious experiment” stage. It is not universal, and it is definitely not mature across every workflow, but the direction is clear: legal teams are testing, buying, and normalizing AI faster than most conservative observers expected.

For IP law, the adoption picture is even more interesting. IP practices are full of research, drafting, comparison, classification, monitoring, and portfolio-analysis tasks. Those are exactly the kinds of workflows where AI can help quickly, as long as attorneys keep human review, confidentiality controls, and professional judgment in the loop.

The adoption baseline

The best public legal-industry adoption data points now cluster around the same story.

The ABA’s 2024 Legal Technology Survey found that 30% of responding lawyers were using AI, up sharply from 11% in 2023. Adoption was higher in larger firms: 46% of firms with 100 or more attorneys reported AI use, compared with 30% of firms with 10 to 49 lawyers and 18% of solo attorneys. (ABA Journal)

Thomson Reuters’ 2025 Generative AI in Professional Services research found adoption at 28% for law firms and 23% for corporate legal departments, while noting that the legal industry was leading GenAI adoption among professional-services groups. (Thomson Reuters)

In-house legal departments are catching up quickly. ACC and Everlaw reported that active GenAI use among corporate legal departments jumped to 52% in 2025, up from 23% in 2024. The same survey found that 64% of in-house counsel expect GenAI to reduce reliance on outside counsel, 50% expect lower outside-counsel costs, and 61% plan to push for changes in how law firms using GenAI deliver and price legal services. (Everlaw, ACC)

That last number matters. Adoption is no longer just a law firm productivity story. It is becoming a client-pricing story.

What adoption looks like in IP law

There is no single public survey that cleanly measures “AI adoption inside IP law firms only.” So the most honest approach is to combine broad legal-industry adoption data with an IP-specific workflow model.

The practical read is this:

IP lawyers are most likely to use AI first in research, drafting support, portfolio review, trademark and brand monitoring, invention intake, and client reporting. They are less likely to use AI without heavy review in high-stakes claim strategy, inventorship analysis, privilege decisions, litigation arguments, enforceability opinions, and settlement strategy.

In other words, AI is already useful in IP. But the value is not “replace the lawyer.” The value is “compress the first 60% of the work so the lawyer can spend more time on judgment.”

Modeled AI adoption by segment

The following estimates are planning assumptions for IP law, built from the public adoption anchors above and adjusted for IP workflow fit.

| Segment | Estimated current AI adoption | Likely first use cases |

|---|---|---|

| Solo IP and small firms | 18% to 28% |

Drafting

Research

Intake

Client updates

Trademark support

|

| Boutique IP firms | 30% to 45% |

Patent drafting support

Office actions

Prior art

Portfolio analytics

|

| Mid-market firms | 28% to 40% |

Research

Litigation support

Licensing review

Diligence

|

| AmLaw and large firms | 40% to 60% |

Enterprise AI

Knowledge management

Research

Litigation

Diligence

|

| In-house legal departments | 45% to 55% |

Portfolio visibility

Outside counsel management

Contract review

Brand monitoring

|

| ALSPs and legal ops providers | 50% to 70% |

Monitoring

Review

Workflow automation

Managed IP operations

|

Modeled adoption by AI tool category

| Tool category | Estimated current adoption in IP workflows | Maturity |

|---|---|---|

| Generative AI drafting and summarization | 30% to 45% | Fast-growing |

| AI legal research | 35% to 55% | Most mature |

| Workflow automation | 25% to 40% | Growing |

| Patent and trademark analytics | 25% to 45% | Strong IP fit |

| Portfolio intelligence | 20% to 35% | Emerging into mainstream |

| Predictive litigation analytics | 10% to 25% | Useful but higher risk |

| Client intake AI | 15% to 30% | Common in consumer and SMB legal markets |

| Compliance and monitoring AI | 20% to 40% | Strong growth in brand and regulatory monitoring |

The center of gravity is shifting from “AI as a better search box” to “AI as a workflow layer.” That shift is what will change staffing, pricing, and client expectations.

Adoption by Firm Size

Tool Category Usage

Budget Allocation Trends

5. Workflow Decomposition Analysis

This is where AI disruption becomes concrete.

It is easy to say “AI will change IP law.” That sounds big, but vague. The useful question is smaller and sharper: which parts of the IP workflow actually absorb time, create cost, and lend themselves to AI support?

IP law is not one workflow. It is a chain of linked activities: intake, search, analysis, drafting, review, filing, prosecution, negotiation, monitoring, litigation, reporting, and billing. Some of those tasks are judgment-heavy. Others are structured, repetitive, and document-heavy. AI does its best work in the second group, especially when a lawyer supervises the output.

The core finding: AI has the highest near-term impact where work is repeatable, text-heavy, search-heavy, or comparison-heavy. It has the lowest safe automation potential where the work depends on strategy, privilege, inventorship, claim scope, settlement posture, client counseling, or courtroom judgment.

Workflow map

For an IP practice, the end-to-end workflow can be broken into nine major workstreams:

- Client intake and matter scoping

This includes new client intake, conflict checks, invention disclosure intake, trademark questionnaires, copyright claim details, brand-enforcement requests, and early matter triage.

AI can help convert messy client inputs into structured summaries. It can flag missing information, route matters by type, draft intake notes, and prepare first-pass issue lists.

The risk is that intake can miss facts that later matter. A weak invention disclosure, an incomplete chain-of-title note, or a misunderstood first-use date can create downstream problems. Human review remains essential.

Estimated time allocation: 6% to 9% of IP workflow time

Estimated AI automation potential: 35% to 55%

Risk exposure if automated: Medium

Cost reduction opportunity: Moderate to high

- Research and search

This is one of the clearest AI opportunities. In IP, research includes prior art search, patentability review, freedom-to-operate support, invalidity research, case law research, trademark clearance, marketplace scans, ownership research, and regulatory or standards-adjacent research.

AI is valuable because it can compress search, summarize large result sets, cluster references, compare claims, and surface related concepts that humans might miss.

The danger is overconfidence. Research tools can miss important references, misunderstand claim language, or present weak matches as strong ones. Lawyers still need to verify the sources and apply judgment.

Estimated time allocation: 16% to 22%

Estimated AI automation potential: 45% to 65%

Risk exposure if automated: High

Cost reduction opportunity: High

- Drafting

Drafting is where clients will expect visible speed gains. Patent application sections, office-action responses, trademark responses, demand letters, cease-and-desist letters, licensing summaries, claim charts, litigation research memos, and portfolio reports can all start faster with AI.

But drafting in IP is dangerous when the model sounds confident and gets technical details wrong. A patent claim can be narrowed accidentally. A trademark argument can cite the wrong standard. A license clause can shift risk. A litigation filing can overstate a point.

The best use case is not unsupervised drafting. It is lawyer-led drafting acceleration.

Estimated time allocation: 22% to 30%

Estimated AI automation potential: 40% to 60%

Risk exposure if automated: High

Cost reduction opportunity: Very high

- Review and analysis

Review sits between raw output and legal judgment. It includes reviewing prior art, comparing claim elements, reviewing examiner rejections, analyzing contracts, checking prosecution history, reviewing evidence, summarizing discovery, and comparing portfolio assets.

AI can help organize the review, but it should not be the final reviewer. In IP, tiny differences matter. A single claim limitation, filing date, ownership gap, prior disclosure, or license carveout can change the answer.

Estimated time allocation: 12% to 18%

Estimated AI automation potential: 30% to 50%

Risk exposure if automated: High

Cost reduction opportunity: Moderate to high

- Negotiation and transaction support

AI can support licensing, coexistence agreements, settlement discussions, M&A diligence, joint-development agreements, SaaS/IP clauses, royalty terms, and indemnity review.

This is less about replacing negotiation and more about improving preparation. AI can compare clauses, summarize issues, benchmark terms, flag unusual provisions, and draft negotiation points.

The human lawyer still owns leverage, tone, business context, and risk allocation.

Estimated time allocation: 7% to 11%

Estimated AI automation potential: 20% to 35%

Risk exposure if automated: Medium to high

Cost reduction opportunity: Moderate

- Compliance, monitoring, and enforcement

This is one of the strongest long-term AI use cases. Brand owners, IP-heavy companies, and in-house teams need to monitor marketplaces, social platforms, app stores, domain registrations, competitor filings, patent landscapes, product launches, and content misuse.

AI can watch more surfaces than a human team can. It can classify likely infringements, rank severity, route matters, generate takedown drafts, and track repeat offenders.

The risk is false positives and false negatives. Over-enforcement can create reputational problems. Under-enforcement can weaken protection or miss commercial harm.

Estimated time allocation: 8% to 13%

Estimated AI automation potential: 45% to 70%

Risk exposure if automated: Medium

Cost reduction opportunity: High

- Litigation support

IP litigation includes case research, claim construction support, invalidity contentions, infringement charts, discovery review, expert materials, damages analysis, deposition preparation, and settlement modeling.

AI can speed up the machinery around litigation. It can organize documents, summarize testimony, find patterns, build chronologies, draft shells, and compare positions.

But litigation strategy cannot safely be delegated. Predictive tools can be helpful, but they can also create false precision. Judges, venues, facts, experts, procedural posture, budgets, and business goals all matter.

Estimated time allocation: 10% to 18%

Estimated AI automation potential: 25% to 45%

Risk exposure if automated: Very high

Cost reduction opportunity: Moderate to high

- Client communication and reporting

IP clients increasingly want clean, frequent, business-friendly updates. They want to know what changed, what matters, what it costs, what comes next, and what the legal team recommends.

AI can produce portfolio summaries, status reports, executive briefs, board-ready updates, matter timelines, and outside counsel reports. This is one of the best client-experience opportunities because it turns legal work into business intelligence.

The risk is oversimplification. A clean summary can hide uncertainty. Lawyers need to make sure client-facing reports do not flatten nuance too much.

Estimated time allocation: 7% to 10%

Estimated AI automation potential: 40% to 60%

Risk exposure if automated: Medium

Cost reduction opportunity: Moderate to high

- Billing, budgeting, and pricing

AI can help analyze matter budgets, compare estimated vs actual time, detect write-off patterns, flag low-margin work, and support fixed-fee pricing.

This workflow matters because AI creates pressure on hourly billing. If drafting takes less time, clients may expect lower bills. Firms that understand matter economics can redesign pricing before clients force the issue.

Estimated time allocation: 4% to 7%

Estimated AI automation potential: 35% to 55%

Risk exposure if automated: Low to medium

Cost reduction opportunity: Moderate

Billable Hours vs Automation Potential

lower AI exposure

high AI exposure

lower AI exposure

high AI exposure

comms

Time Savings Model (before vs after AI)

6. Revenue Model Sensitivity Analysis

AI does not disrupt every IP revenue model in the same way.

That matters because two firms can use the same AI tool and get opposite economic outcomes. One firm may lose billable hours. Another may expand margins. A third may win more work by offering faster turnaround and better reporting. The technology is only half the story. The pricing model decides who captures the value.

The core issue is simple: AI compresses time. Under hourly billing, time compression can reduce revenue. Under flat-fee or subscription models, time compression can increase margin. Under contingency or success-fee models, AI mostly improves screening, evidence organization, and case selection.

The basic revenue problem

A large share of IP work still depends on hourly billing or time-based budgeting. That creates a built-in tension.

If a patent office-action response usually takes 10 hours and AI helps reduce the work to 6.5 hours, the client may expect the bill to fall. If the firm bills hourly, revenue falls unless the firm replaces those hours with more matters, higher-value work, or alternative pricing.

But if the same matter is priced as a fixed-fee response, the economics flip. The firm can keep the same fee, reduce production time, and improve margin, assuming quality stays high.

That is why AI strategy cannot be separated from pricing strategy.

Revenue model exposure

Hourly billing is the most exposed model because the firm sells time. When AI reduces time, it directly pressures revenue. This does not mean hourly billing disappears. Complex litigation, opinions, high-stakes licensing, and strategic counseling will still use hourly or hybrid models. But routine drafting, research, monitoring, reporting, and repeatable prosecution work will be harder to defend as pure hourly work.

Fixed-fee work is the most obvious margin winner. Patent prosecution, trademark filings, office-action responses, portfolio audits, licensing templates, and enforcement packages can become more profitable if AI reduces production cost while the firm maintains price discipline.

Subscription models become more viable because AI lowers the cost of recurring service delivery. Brand monitoring, portfolio reporting, competitive intelligence, startup IP support, outside counsel dashboards, and basic enforcement triage can be packaged as monthly or quarterly services.

Contingency and success-fee models are less exposed to time compression and more affected by better selection. AI can help identify stronger infringement claims, organize evidence faster, evaluate invalidity risk, estimate damages ranges, and decide whether a matter deserves investment.

Hybrid and alternative-fee models may become the most attractive middle ground. They let firms protect upside while giving clients a visible answer to the question: “How is AI changing what I pay?”

Base model: 35% drafting-time automation

For sensitivity modeling, assume a drafting-heavy IP matter with the following baseline:

Total matter time: 100 hours

Drafting share: 26 hours

Billing rate: $450 per hour

Baseline hourly revenue: $45,000

AI automation scenario: 35% of drafting time is eliminated or compressed

Drafting time saved: 9.1 hours

New matter time: 90.9 hours

New hourly revenue: $40,905

Revenue compression under hourly billing: $4,095

Revenue decline: 9.1%

This is the uncomfortable math. A tool that makes the firm more efficient can make the matter less valuable under a pure hourly model.

Scenario 1: Hourly billing

Under hourly billing, AI savings pass through to the client unless the firm changes the commercial structure.

A 35% reduction in drafting time on a 100-hour matter reduces total matter hours by 9.1%. At a $450 hourly rate, that is a $4,095 revenue reduction.

That may be acceptable if the firm can handle more matters with the same team. But if demand does not increase, the firm simply becomes more efficient while earning less.

The risk is highest for repeatable work such as:

- Office-action response drafts

- Trademark response drafts

- Claim-chart shells

- Licensing first drafts

- Prior art summaries

- Portfolio reports

- Client update memos

The strategic fix is not to avoid AI. That would be a losing move. The fix is to redesign pricing around output, speed, and value.

Scenario 2: Fixed-fee pricing

Now take the same matter and assume it is priced as a fixed fee.

Fixed fee: $45,000

Original labor cost: 100 hours × $180 internal cost per hour = $18,000

Original gross margin: $27,000

Original margin rate: 60.0%

After AI: 90.9 hours × $180 internal cost per hour = $16,362

Revenue stays: $45,000

New gross margin: $28,638

New margin rate: 63.6%

Margin expansion: 3.6 percentage points

The client gets faster turnaround. The firm gets better margin. This is the cleanest AI economic model, as long as the firm can maintain quality and avoid underpricing the work.

Scenario 3: Fixed fee with client discount

Some clients will expect AI savings to be shared. That does not have to be bad.

Assume the firm offers a 5% AI-enabled efficiency discount.

Discounted fixed fee: $42,750

After-AI labor cost: $16,362

Gross margin: $26,388

Margin rate: 61.7%

Even with a 5% discount, the firm’s margin rate remains higher than the original 60.0% baseline. The client sees savings. The firm protects profitability. This kind of shared-savings model may become common in repeatable IP work.

Scenario 4: Subscription model

AI also makes recurring IP services easier to package.

A subscription model might include:

- Monthly trademark watch reports

- Quarterly patent portfolio summaries

- Competitor filing alerts

- Office-action triage

- Executive IP dashboards

- Marketplace enforcement scans

- Outside counsel spend reporting

The economics depend on volume. If AI lowers the cost of each report, alert, or review cycle, a firm can serve more clients with the same team.

Example:

Monthly subscription price: $6,000

Manual delivery cost: $3,900

Manual gross margin: $2,100

Manual margin rate: 35%

AI-assisted delivery cost: $2,700

AI-assisted gross margin: $3,300

AI-assisted margin rate: 55%

This is why subscription IP services are attractive. They turn irregular billable work into recurring revenue, and AI improves delivery economics.

Scenario 5: Contingency or success-fee work

AI is less likely to compress revenue in contingency work because the firm is not selling hours. Instead, AI improves matter selection.

In IP enforcement, litigation finance, licensing campaigns, and damages-driven disputes, AI can help answer:

Is the patent likely valid?

Is infringement plausible?

Are there comparable licenses?

What products are implicated?

How strong is the claim chart?

What defenses are likely?

What is the likely cost to pursue?

What is the settlement range?

Better screening can reduce wasted effort. It can also help firms avoid weak matters and focus resources on claims with stronger expected value.

The impact is not lower revenue per hour. It is better portfolio selection.

Revenue compression vs margin expansion

The strategic split looks like this:

Hourly billing turns AI savings into client savings unless the firm changes pricing or increases volume.

Fixed-fee billing turns AI savings into firm margin unless the firm discounts.

Subscription billing turns AI savings into scalable recurring revenue.

Contingency billing turns AI savings into better case selection and lower pursuit cost.

Hybrid billing lets the firm share savings while preserving upside.

The firms that win will not simply ask, “How many hours can AI save?” They will ask, “Who captures the value of those saved hours?”

Revenue Compression Model

Margin Expansion Model

7. Competitive AI Vendor Landscape

The AI vendor landscape for IP law is crowded, uneven, and moving fast.

It is not one market. It is a stack of overlapping markets: legal research AI, drafting copilots, patent analytics, trademark monitoring, IP management systems, litigation analytics, intake automation, contract AI, and enterprise legal AI platforms. Some vendors are pure legal AI companies. Some are legacy legal-data giants adding AI to existing platforms. Others are IP operations platforms that are quietly becoming AI-enabled workflow systems.

For IP law, the real competitive question is not “Which vendor has the best chatbot?”

The better question is: “Which vendor controls the workflow, the data, the legal content, and the trusted system of record?”

That is where durable advantage sits.

Market structure

The AI-for-IP vendor landscape has four layers.

First, there are legal AI platforms. These are broad copilots and agentic workspaces that help lawyers research, summarize, draft, review, and manage legal work. Harvey, Legora, Thomson Reuters CoCounsel, LexisNexis Protégé, and Eudia sit in or near this layer.

Second, there are IP intelligence platforms. These tools focus on patents, trademarks, innovation data, competitive intelligence, portfolio analytics, and technology landscapes. PatSnap, Clarivate, Anaqua, Questel, and similar platforms are especially relevant here.

Third, there are workflow and matter-specific tools. These vendors focus on a narrower wedge: contracts, intake, litigation support, eDiscovery, demand letters, docketing, enforcement, or managed services.

Fourth, there are enterprise infrastructure players. Microsoft, OpenAI, Google, AWS, and Anthropic do not sell “IP law” products in the narrow sense, but their models and cloud systems power many legal AI deployments.

Category 1: Legal research AI

This is the most mature legal AI category because lawyers already pay for research platforms, and the output can be checked against legal sources.

Key vendors include Thomson Reuters CoCounsel, LexisNexis Protégé, vLex Vincent AI, Bloomberg Law AI tools, and Harvey’s research workflows. Thomson Reuters launched CoCounsel Legal with Deep Research and agentic guided workflows in 2025, explicitly positioning it as a move from prompting toward delegated professional workflows. (Thomson Reuters)

LexisNexis has positioned Protégé as a personalized AI assistant with agentic AI for complex legal task completion, while emphasizing its grounding in the LexisNexis legal corpus. (LexisNexis)

For IP law, research AI touches case law, claim construction, patent validity research, office-action research, trademark refusals, licensing standards, damages research, and litigation strategy support.

Likely winners are vendors with trusted legal corpora, citation validation, workflow integrations, and enterprise-grade security. This favors incumbents, but startups can still win if they build better workflows on top of trusted data.

Category 2: Contract analysis and licensing AI

Contract AI matters for IP because licensing is contract-heavy. AI can help review licensing agreements, coexistence agreements, software agreements, R&D agreements, joint-development agreements, assignment agreements, SaaS terms, indemnities, royalty provisions, and ownership clauses.

Key vendors include Ironclad, Icertis, LinkSquares, Luminance, Evisort, Kira, and broader legal AI platforms that handle contract review. For IP practices, the most valuable features are clause extraction, royalty-term comparison, ownership-risk flagging, indemnity review, change-of-control analysis, open-source software review, and diligence summaries.

This category is mature enough that buyers understand it, but IP-specific differentiation still matters. A generic contract AI system can summarize a license. A strong IP-focused system should understand field-of-use restrictions, sublicensing rights, prosecution control, enforcement obligations, assignment gaps, background IP, foreground IP, and royalty audit provisions.

Category 3: Patent and trademark analytics

This is the core IP-specific software layer.

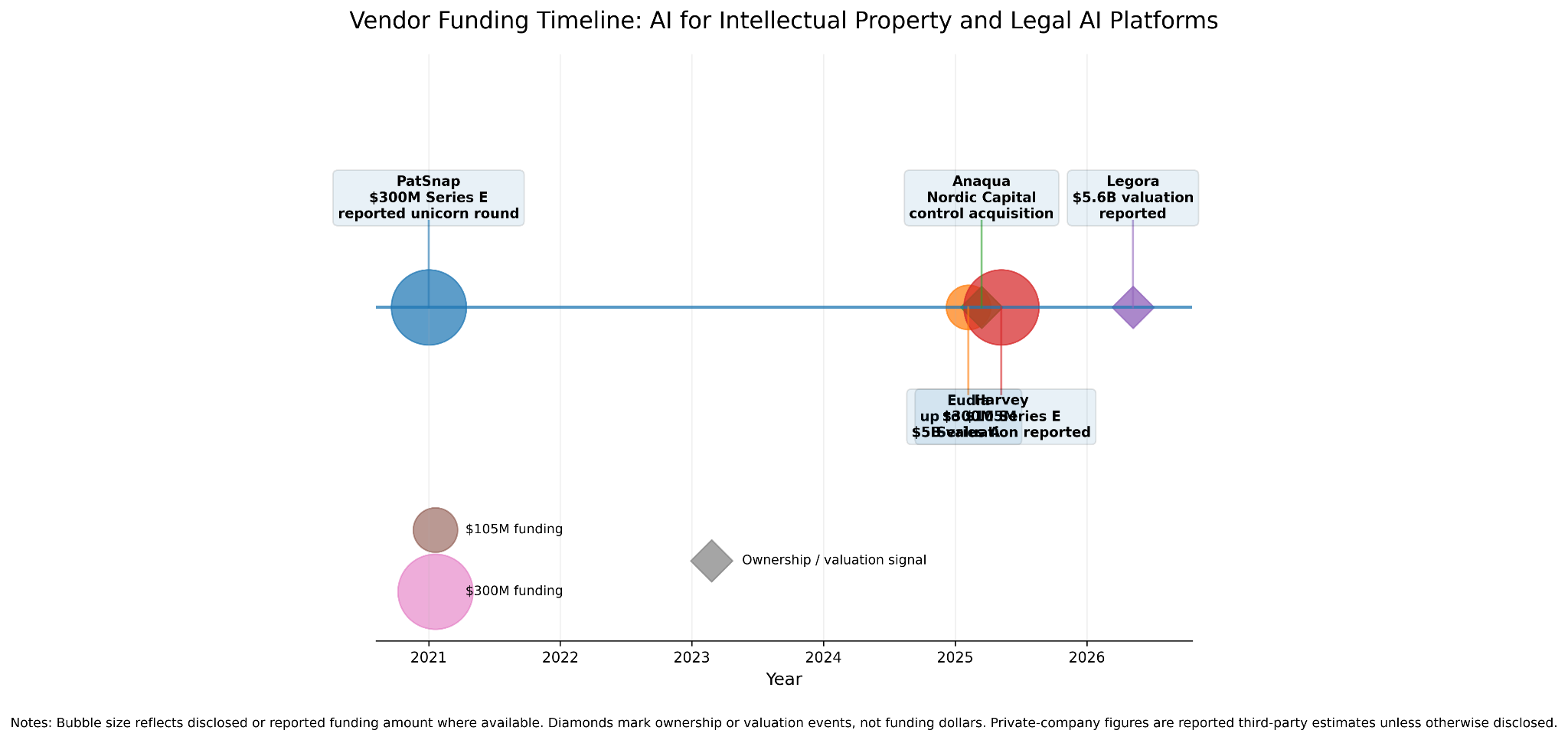

Vendors include PatSnap, Clarivate, Anaqua, Questel, IP.com, LexisNexis PatentSight, Minesoft, and other patent-data platforms. PatSnap is an especially important example because it is built around AI-driven patent search and IP intelligence. Tracxn lists PatSnap as having raised about $352 million and reaching a $1 billion valuation, though those figures should be treated as third-party private-market estimates rather than audited financials. (Tracxn)

Anaqua is also important because it sits close to the system-of-record layer for IP management. In February 2025, Nordic Capital completed its acquisition of a controlling interest in Anaqua, describing the company as a provider of innovation and IP management technology solutions and services. (Anaqua)

Clarivate remains a major IP-data and analytics player. Its 2024 annual report describes the company as supporting the innovation, knowledge, and research lifecycle across Academia & Government, Intellectual Property, and Life Sciences & Healthcare. (SEC)

For IP law, patent and trademark analytics vendors compete on data coverage, search quality, entity resolution, family mapping, claims analytics, competitor intelligence, litigation data, citation mapping, valuation support, and workflow depth.

The strongest vendors in this segment are not just selling AI. They are selling curated IP datasets plus analytical workflows. That is harder to replicate than a generic drafting assistant.

Category 4: Litigation prediction and analytics

Litigation analytics has real value in IP, but it is a higher-risk category.

Vendors include Lex Machina, Westlaw analytics, Bloomberg Law litigation analytics, Premonition, Solomonic, Trellis, and newer AI-enabled litigation tools. For IP litigation, the relevant workflows include venue analysis, judge analytics, opposing counsel behavior, damages patterns, claim construction outcomes, motion trends, settlement modeling, and PTAB analytics.

The market opportunity is attractive, but buyers are cautious. A litigation prediction model can look precise while missing the facts that actually decide a case. The strongest use case is decision support, not autonomous prediction.

In IP litigation, these tools are best used to frame questions:

How has this judge handled claim construction?

How often do similar motions succeed?

What venues move fastest?

How does this opposing counsel behave?

What damages theories have survived?

What PTAB patterns matter?

The output should inform strategy, not replace it.

Category 5: Compliance, monitoring, and enforcement AI

This category is especially important for trademarks, copyrights, counterfeiting, digital content, and brand protection.

Vendors include Corsearch, Red Points, Pointer Brand Protection, MarkMonitor, Clarivate trademark tools, online marketplace monitoring platforms, and internal AI systems built by large brand owners.

AI can monitor marketplaces, social media, app stores, domain registrations, search ads, product listings, competitor filings, and infringing content. It can triage likely violations, rank severity, draft takedown notices, and identify repeat offenders.

This segment has strong economic logic because monitoring is repetitive, high-volume, and hard for humans to do comprehensively. The risk is over-enforcement or false positives, especially in fair use, parody, resale, gray market, and descriptive-use contexts.

Category 6: Drafting copilots

Drafting copilots are one of the fastest-growing categories in legal AI.

Vendors include Harvey, Spellbook, Legora, LexisNexis Protégé, CoCounsel, Microsoft Copilot-based legal deployments, and practice-specific drafting tools. Harvey is the best-known legal AI startup in this segment. Reports in 2025 described Harvey raising a $300 million Series E at a $5 billion valuation, and later reports said it crossed $100 million in ARR. Because Harvey is private, ARR figures should be treated as reported figures, not audited public-company disclosures. (TechFundingNews, TechStartups)

Legora is another major legal AI platform to watch. TechCrunch reported in April 2026 that Legora reached a $5.6 billion valuation, highlighting direct competition with Harvey. (TechCrunch)

For IP law, drafting copilots can support invention disclosure summaries, office-action response drafts, trademark refusal responses, licensing summaries, claim-chart shells, cease-and-desist letters, client updates, and litigation memo drafts. The market risk is commoditization. A generic drafting assistant is easy to swap out. A drafting assistant embedded into IP data, docketing, templates, prior art, and client playbooks is much harder to replace.

Category 7: Case intake AI

Case intake AI is more mature in consumer and plaintiff-side legal markets than in high-end IP law, but the workflow still matters.

For IP, intake AI can structure invention disclosures, trademark questionnaires, brand-enforcement requests, copyright claims, startup IP assessments, and early litigation triage. The buyer is often a solo firm, small firm, boutique practice, or in-house team trying to avoid messy intake emails and incomplete client submissions.

Vendors include general legal intake platforms, chatbot tools, CRM-integrated legal automation systems, and custom firm-built workflows. The strongest IP use case is not a public-facing “legal advice bot.” It is guided intake that captures the facts lawyers need while reducing back-and-forth.

Category 8: Legal analytics and enterprise legal platforms

This layer overlaps with everything else. It includes Eudia, enterprise legal management systems, spend management tools, matter management platforms, knowledge management systems, and AI-enabled dashboards.

Eudia is notable because it targets corporate legal teams and secured up to $105 million in Series A funding in 2025, led by General Catalyst. The company describes itself as an augmented intelligence platform for Fortune 500 legal teams. (PR Newswire)

Business Insider later reported that Eudia acquired Johnson Hana and noted Eudia was generating more than $10 million in ARR and was on track to double by year-end. That is a media-reported private-company figure, not audited disclosure, but it is still useful as a directional market signal. (Business Insider)

For IP-heavy corporate departments, this category matters because in-house teams want visibility: portfolio status, spend, outside counsel performance, risks, deadlines, enforcement matters, and board-ready summaries.

Funding picture

The funding environment shows a clear split.

Broad legal AI platforms are attracting huge rounds and valuations because investors see them as potential operating systems for legal work. Harvey and Legora are the clearest examples. Harvey’s reported $300 million Series E at a $5 billion valuation and Legora’s reported $5.6 billion valuation show how aggressively investors are underwriting enterprise legal AI. (TechFundingNews, TechCrunch)

Corporate legal AI platforms are also getting funded, but with a different thesis. Eudia’s $105 million Series A is less about giving lawyers a chatbot and more about rebuilding how corporate legal work gets routed, managed, and augmented. (PR Newswire)

IP-specific platforms have a more data-and-workflow-heavy advantage. Anaqua’s 2025 sale to Nordic Capital shows that private equity still sees value in IP management systems, especially those that can become AI-enabled systems of record. (Anaqua)

Market share estimate

Precise market share is not publicly available for AI-for-IP specifically. The market is too fragmented, and many vendors do not report AI-specific or IP-specific revenue.

A useful planning estimate is to split the market by influence rather than reported revenue:

Legal-data incumbents: 35% to 45% influence share

IP management and analytics platforms: 25% to 35%

Enterprise legal AI startups: 15% to 25%

Brand protection and monitoring platforms: 8% to 15%

Point-solution vendors and firm-built tools: 5% to 10%

This is not a revenue market share table. It is a strategic influence estimate, based on customer access, data control, workflow depth, and platform position.

Differentiation factors

The winning vendors will not win because their model writes prettier paragraphs. They will win because they solve harder problems.

The key differentiators are:

- Trusted legal and IP data

- Citation validation and source grounding

- Patent and trademark corpus depth

- Docketing and matter integration

- Document-management integration

- Security and confidentiality controls

- Client-specific playbooks

- Workflow automation, not just chat

- Audit logs and governance

- Human review design

- Output quality in narrow IP tasks

- Enterprise procurement readiness

For IP law, data depth may be the most important moat. Generic AI can draft a memo. It cannot easily recreate decades of patent, trademark, litigation, citation, docket, assignment, family, claim, and prosecution data.

Vendor Funding Timeline

Market Share Estimate

AI Vendor Positioning Matrix (Enterprise vs SMB)

platform depth

and system of record

and automation

solutions

8. Disruption Vectors

AI will not disrupt IP law all at once. It will move through the practice in waves.

The first wave is already here: faster research, faster first drafts, better summarization, and cleaner portfolio visibility.

The second wave is underway: AI connected to docketing, matter management, document systems, client reporting, and outside counsel management.

The third wave is the one firms should prepare for now: AI-native service models where IP work is sold as fixed-fee packages, subscriptions, dashboards, alerts, and managed services instead of only hourly labor.

The major disruption vectors are:

- Research compression

- Drafting automation

- Predictive litigation modeling

- Client intake automation

- Risk monitoring and compliance AI

- Billing transparency and AI-driven pricing

The common thread is simple: AI compresses the production layer of IP work, then forces everyone to rethink pricing, staffing, and client value.

1. Research compression

Research compression is the most immediate disruption vector.

IP lawyers spend enormous time searching, comparing, and synthesizing information: prior art, patents, prosecution histories, examiner behavior, trademark records, litigation history, ownership records, technical references, case law, and competitor portfolios.

AI changes the speed of that work. It can summarize large document sets, cluster references, compare claim elements, produce first-pass research memos, identify similar marks, extract issue patterns, and generate structured summaries from messy data.

In patent work, this can affect:

- Prior art searches

- Patentability reviews

- Freedom-to-operate support

- Invalidity research

- Claim construction support

- Prosecution-history review

- Competitor portfolio analysis

In trademark work, it can affect:

- Clearance searches

- Likelihood-of-confusion screening

- Office-action research

- Marketplace review

- Brand similarity analysis

In litigation, it can affect:

- Case law review

- Judge and venue research

- Motion pattern analysis

- Claim chart support

- Damages research

The economic impact is direct. Research hours become harder to justify when AI-assisted tools can surface and summarize relevant material quickly. That does not eliminate attorney judgment. It changes where the lawyer spends time.

Current maturity: High for assisted research, medium for final legal analysis

Time to mainstream: Already mainstreaming through 2026 to 2028

Economic impact: High

Primary risk: Missed sources, shallow analysis, hallucinated citations, overconfidence

Strategic implication: Firms need research protocols that combine AI speed with human verification.

Legal research AI is already one of the most mature legal AI categories because it fits an existing lawyer workflow and can be grounded in source materials. Thomson Reuters and LexisNexis have both moved aggressively into AI-assisted and agentic legal research products, which signals that research compression is now part of the mainstream legal platform race. (Thomson Reuters, LexisNexis)

2. Drafting automation

Drafting automation is the most visible disruption vector because clients can feel it.

A task that once took a lawyer a day may now produce a rough first draft in minutes. That changes expectations, even when the final work still requires careful review.

In IP law, drafting automation touches:

- Invention disclosure summaries

- Patent specification sections

- Claim-drafting support

- Office-action response drafts

- Trademark refusal responses

- Cease-and-desist letters

- Licensing summaries

- Coexistence agreements

- Claim chart shells

- Invalidity-contention drafts

- Client update memos

- Portfolio summaries

- Board-ready IP reports

The danger is that IP drafting is not ordinary writing. Tiny choices matter. A claim term can narrow scope. A prosecution argument can create estoppel. A licensing clause can shift commercial risk. A trademark response can frame the record poorly. A litigation draft can overstate the law.

So the real opportunity is not “AI writes the final work product.” The opportunity is “AI makes the first version faster, and lawyers spend more time on strategy, review, and judgment.”

Current maturity: Medium to high for first drafts and summaries

Time to mainstream: 2026 to 2029

Economic impact: Very high

Primary risk: Technical errors, overbroad language, narrowing amendments, confidentiality exposure, weak legal reasoning

Strategic implication: Firms should create approved drafting playbooks, review checklists, and matter-type templates.

The economic issue is serious. Drafting is often one of the largest time blocks in IP work. If AI compresses drafting time under hourly billing, the firm can lose revenue. If the same work is fixed-fee, the firm can expand margin.

That is the pricing inversion.

3. Predictive litigation modeling

Predictive litigation modeling is powerful, but risky.

IP litigation has enough structured data to support analytics: courts, judges, venues, patent types, motion outcomes, damages awards, PTAB results, opposing counsel, claim construction outcomes, and settlement patterns.

AI can help answer practical questions:

How does this judge handle claim construction?

How often do similar motions succeed?

What is the likely time to trial?

What venues create leverage?

What damages theories survived in similar matters?

Which prior art references appear strongest?

How often does this patent owner settle?

How has this opposing counsel behaved before?

Which PTAB patterns matter?

The upside is better early case assessment. A firm can screen matters faster, set budgets more intelligently, improve settlement posture, and avoid weak claims.

But predictive litigation tools can create false precision. A model can show a probability, but litigation is not a weather forecast. Witnesses, experts, business goals, budgets, injunction risk, venue strategy, privilege issues, and judge-specific facts all matter.

Current maturity: Medium for analytics, early-to-medium for reliable prediction

Time to mainstream: 2027 to 2030 for decision support, longer for high-trust prediction

Economic impact: Moderate to high

Primary risk: False precision, bias, incomplete datasets, overreliance, client misunderstanding

Strategic implication: Use predictive tools to frame decisions, not to make decisions.

This area will likely remain attorney-led. The best firms will use predictive analytics as a strategic dashboard, not as a substitute for litigation judgment.

4. Client intake automation

Client intake automation is less flashy than litigation prediction, but it can reshape the front door of IP practice.

IP matters often begin with messy inputs:

- An inventor sends a rough technical description

- A founder asks whether an idea is patentable

- A brand team wants to clear a name

- A marketing team finds a counterfeit listing

- An employee leaves with sensitive files

- A client asks whether a competitor’s product infringes

- A business unit wants to license technology

- A litigation lead arrives with partial facts

AI can structure those inputs. It can ask follow-up questions, collect missing facts, classify the matter, route it to the right team, create a matter summary, estimate complexity, and prepare a lawyer for the first call.

For patent work, intake AI can improve invention disclosure quality. For trademark work, it can capture first-use dates, goods and services, target markets, specimen issues, and known conflicts. For enforcement, it can collect URLs, screenshots, product details, seller names, and prior communications.

Current maturity: Medium in general legal intake, early-to-medium in IP-specific intake

Time to mainstream: 2026 to 2028 for structured intake, 2028 to 2030 for deeper triage

Economic impact: Moderate

Primary risk: Missing key facts, unauthorized legal advice, bad matter classification, confidentiality issues

Strategic implication: Intake AI should be guided, narrow, and supervised. It should collect facts, not give final legal advice.

The biggest value is not replacing the first lawyer conversation. It is making that conversation better. Cleaner intake means fewer emails, fewer gaps, faster scoping, and better pricing.

5. Risk monitoring and compliance AI

Risk monitoring may become one of the most valuable long-term AI use cases in IP.

Why? Because IP risk does not wait for office hours.

Brands are copied on marketplaces. Counterfeit sellers move quickly. Competitors file patents quietly. Domains are registered. Apps appear. Content is scraped. Products launch. Employees leave. Open-source code enters products. Trade secrets spread. New regulations affect AI-generated content, copyright, privacy, and data governance.

Humans cannot watch all of that manually.

AI can monitor:

- Online marketplaces

- Social platforms

- App stores

- Domain registrations

- Advertising

- Competitor patent filings

- Trademark filings

- Product launches

- Software repositories

- Copyright misuse

- Counterfeit listings

- Gray-market activity

- Trade-secret risk signals

- Contract compliance

- Licensing obligations

For brand owners and IP-heavy companies, monitoring AI shifts IP work from reactive to proactive. The legal team can catch problems earlier, rank severity, and decide which matters deserve action.

Current maturity: Medium to high for brand monitoring, medium for broader IP compliance

Time to mainstream: 2026 to 2029

Economic impact: High

Primary risk: False positives, over-enforcement, missing context, fair use errors, reputational risk

Strategic implication: Firms can package monitoring as a subscription or managed service.

This is one of the clearest places where AI expands the market instead of only reducing hours. A client that could not afford broad monitoring may buy a lower-cost AI-enabled monitoring package. A firm that used to handle only enforcement actions can now offer continuous brand protection.

6. Billing transparency and AI-driven pricing

This may be the most commercially disruptive vector.

Clients are already asking why legal work should cost the same if AI makes it faster. In-house teams are under pressure to control spend, and they can now credibly ask outside counsel how AI affects matter staffing, timelines, and price.

The question will not be theoretical. It will show up in RFPs, billing guidelines, outside counsel reviews, and panel negotiations.

Clients will ask:

Did you use AI on this matter?

What work did AI accelerate?

How did you supervise it?

Did it reduce hours?

Did those savings affect the bill?

Can this work be fixed-fee?

Can we get a subscription for monitoring?

Can you provide a dashboard instead of a memo?

Can we bring the first-pass work in-house?

This is where AI changes law firm economics. The disruption is not just that work gets faster. It is that pricing becomes harder to hide behind time.

Current maturity: Early but accelerating

Time to mainstream: 2026 to 2030

Economic impact: Very high

Primary risk: Revenue compression, client distrust, inconsistent disclosure practices, weak ROI measurement

Strategic implication: Firms need pricing models that let them share efficiency gains without destroying margin.

The in-house pressure is already visible. ACC and Everlaw reported that 64% of in-house counsel expect GenAI to reduce reliance on outside counsel, 50% expect reduced outside counsel costs, and 61% plan to push for changes in how law firms using GenAI deliver and price legal services. (Everlaw, ACC)

9. Case Studies

Case Study 1: Allen & Overy and Harvey

Use case: enterprise legal AI assistant for research, drafting, and internal legal workflows

Allen & Overy was one of the first major global law firms to roll out Harvey at scale. The firm began with a smaller trial, then expanded access across thousands of employees in dozens of offices. Wired reported that Allen & Overy’s use of Harvey had expanded to roughly 3,500 employees across 43 offices, with about 40,000 queries submitted, and that one in four lawyers was using the tool daily. (WIRED)

Why it matters for IP:

Harvey was not built only for IP, but the rollout is important because it shows how large law firms adopt AI: not as a toy, and not as an unsupervised lawyer replacement. The use case is assistant-level work: legal questions, drafting support, summaries, research, and internal productivity.

For IP practices, the transferable lesson is clear. Large firms are willing to deploy AI when the tool fits inside professional workflows and can be governed centrally.

Before AI:

Large-firm associates and professional staff handled first-pass legal research, draft preparation, and document-heavy tasks manually.

After AI:

The firm used Harvey to accelerate legal queries, drafting, and internal support workflows at scale.

Impact:

The clearest public impact is adoption intensity, not a quantified dollar outcome. The reported 3,500-user rollout and 40,000-query volume show real institutional usage, but the public source does not provide audited time savings, revenue impact, or client satisfaction scores. (WIRED)

Analyst read:

This is a strong adoption case study, not a clean ROI case study. It proves that elite law firms will use generative AI in serious legal work. It does not prove that Harvey reduced IP drafting time by a specific percentage.

Case Study 2: Brinks and CoCounsel

Use case: legal AI for research, negotiation support, and reducing work sent to outside counsel

Thomson Reuters published a case study on Brinks, describing how the company used CoCounsel to transform legal workflows. The case study says tasks that previously required external legal support could be handled in-house, with CoCounsel acting as a virtual legal assistant. It also quotes Brinks’ legal leadership saying some AI-supported work is at the level of an associate at a law firm, and that the company could save outside counsel costs. (Thomson Reuters)

Why it matters for IP:

This is directly relevant to IP-heavy clients because in-house teams are the buyers most likely to pressure outside counsel. If they can perform more first-pass research, negotiation preparation, and document review internally, they will send narrower and more strategic questions to law firms.

Before AI:

Some research and negotiation-support work was routed externally.

After AI:

CoCounsel supported internal legal work, helping the team handle more tasks in-house.

Impact:

The public case study describes time savings and reduced outside counsel reliance, but it does not publish a clean percentage reduction in outside counsel spend. The most defensible way to use this case is as evidence of in-house substitution pressure, not as proof of a specific 20% cost reduction. (Thomson Reuters)

Analyst read:

This is one of the most important commercial signals in the report. The disruption is not only law firms using AI. It is clients using AI to avoid sending certain work to law firms in the first place.

Case Study 3: Acuity Law and CoCounsel

Use case: generative AI for drafting and core legal tasks inside a law firm

Thomson Reuters published a CoCounsel case study on Acuity Law, describing the firm as an early adopter of CoCounsel Core and CoCounsel Drafting. The case study says Acuity saw significant time savings in a short period and used the tools to accelerate and improve drafting workflows. (legalsolutions.thomsonreuters.co.uk)

Why it matters for IP:

Acuity is not presented as an IP-only case study, so it should not be overstated. But the workflow is highly relevant. IP practices have many drafting-heavy tasks: office-action responses, licensing summaries, claim charts, trademark responses, cease-and-desist letters, and client updates.

Before AI:

Lawyers handled drafting and routine legal tasks through standard manual workflows.

After AI:

The firm adopted CoCounsel Core and CoCounsel Drafting to speed up legal tasks and drafting.

Impact:

The public source says there were significant time savings, but it does not provide a specific verified percentage in the snippet available. Because of that, this report should not turn the case into “Acuity reduced drafting time by 40%” unless the underlying PDF provides that exact figure. (legalsolutions.thomsonreuters.co.uk)

Analyst read:

This is useful as a law-firm productivity example. It supports the claim that drafting acceleration is real, but not a precise quantitative benchmark.

Case Study 4: Lex Machina and patent litigation analytics

Use case: AI and analytics for patent litigation strategy, venue analysis, timing, damages, judges, parties, and counsel behavior

Lex Machina is one of the clearest examples of AI-enabled litigation analytics in IP. LexisNexis describes Lex Machina as providing legal analytics that combine expert legal knowledge with machine learning to predict behavior of judges, attorneys, parties, and courts. (lexisnexisip.com)

Lex Machina’s 2025 Patent Litigation Report also reported a resurgence in patent filings, design lawsuits, ANDA litigation, and more than $4.3 billion in damages. (LexisNexis)

Why it matters for IP:

Patent litigation is expensive, technical, and data-rich. A tool that helps lawyers understand judges, venues, damages patterns, timing, and motion outcomes can influence case strategy before the first major filing.

Before AI or analytics:

Litigation strategy relied heavily on lawyer experience, manual research, anecdotal knowledge, and traditional case-law review.

After AI-enabled analytics:

Lawyers can use data-backed insights to assess venue, judge behavior, motion timing, damages history, and litigation patterns.

Impact:

The public sources support the existence and use of analytics for litigation strategy, but they do not prove that the tool “predicts outcomes” with a disclosed accuracy rate. This is best framed as litigation decision support, not deterministic prediction. (lexisnexisip.com, iCrowdNewswire)

Analyst read:

This is the right way to talk about predictive litigation AI in IP: helpful, commercially important, but risky if marketed as certainty. Litigation analytics should sharpen strategy, not replace judgment.

Case Study 5: Unilever legal operations and AI-enabled in-house work

Use case: in-house legal delivery centers using AI tools to improve efficiency and reduce external reliance

The Financial Times reported that Unilever’s legal function built legal delivery centers in Barcelona, Mexico City, and Bengaluru to manage high-volume legal work, using tools including Microsoft Copilot and CoCounsel. The report said the legal team saved lawyers an average of about 30 minutes per day and reduced dependency on external counsel. (Financial Times)

Why it matters for IP:

This is not an IP-only case study, but it is highly relevant to the operating model. Large companies with IP-heavy portfolios can use legal delivery centers, AI tools, and standardized workflows to move more repeatable work in-house.

Before AI:

High-volume legal work required more manual effort and more reliance on traditional outside counsel support.

After AI:

Legal delivery centers used AI-supported workflows to improve efficiency and reduce external dependence.

Impact:

Reported lawyer time savings averaged roughly 30 minutes per day. The report also describes reduced dependency on external counsel, but does not provide a specific verified percentage reduction in outside counsel spend. (Financial Times)

Analyst read:

This is the clearest “in-house operating model” example. It shows how AI may shift legal work away from outside counsel even when the legal department does not fully automate the work.

KPI Improvements

Cost Reduction Model

11. Appendix: Data Sources

Primary data sources

The report uses the following public sources as anchor points.

| Source | What it supports | Notes | Category |

|---|---|---|---|

|

Verified Market Research

Open source

|

Global IP law firm services market size | Used as the global IP legal-services market anchor: $14.98B in 2024, projected $46.05B by 2032. | Market sizing |

|

Grand View Research

Open source

|

Global legal AI market size and CAGR | Used as the legal AI market growth benchmark: $1.45B in 2024, projected $3.90B by 2030, 17.3% CAGR. | Market sizing |

|

USPTO OED roster

Open source

|

Patent practitioner count | Used for registered U.S. patent practitioner counts, including patent attorneys and patent agents. | Attorney data |

|

Data.gov USPTO patent practitioner dataset

Open source

|

Scope caveat for trademark attorneys | Important caveat: the USPTO does not maintain a roster of trademark attorneys because trademark attorneys do not need USPTO registration. | Attorney data |

|

ABA 2024 Artificial Intelligence TechReport

Open source

|

Lawyer AI adoption by firm size | Used for broad legal AI adoption benchmarking, including variation between solo practitioners, small firms, and larger firms. | Adoption |

|

ABA Formal Opinion 512

Open source

|

Ethics and professional responsibility | Used for competence, confidentiality, communication, fees, supervision, and candor guidance around generative AI use by lawyers. | Ethics |

|

USPTO AI guidance

Open source

|

AI use in patent and trademark practice | Used for practice before the USPTO, including filings, signatures, confidentiality, candor obligations, and safe use of USPTO systems. | Regulatory |

|

ACC / Everlaw GenAI survey

Open source

|

In-house legal AI adoption and outside counsel pressure | Used for current-state adoption and outside counsel substitution pressure among corporate legal departments. | Adoption |

|

Vendor announcements and credible media reports

Example source

|

Vendor funding, ARR, product launches, and case studies | Used only where public references exist. Private-company numbers are treated as reported estimates unless disclosed directly. | Vendor data |